Publications

Current issue: Fall 2023 v19, n1

A snapshot of Immigration Flows into the US

Armando R. Lopez-Velasco

The US is a rich country to which many people from developing countries would like to migrate to. The opportunities to migrate are restricted to people who fall into certain categories: relatives of US citizens (with priority given to immediate relatives of American citizens but there are permits to other relatives under “family-sponsored” preferences like siblings of American citizens), workers with certain skills (mostly classified as high-skilled), permits for refugees and asylees; and finally there is a “diversity” lottery where people from countries with low rates of immigration to the US can apply.

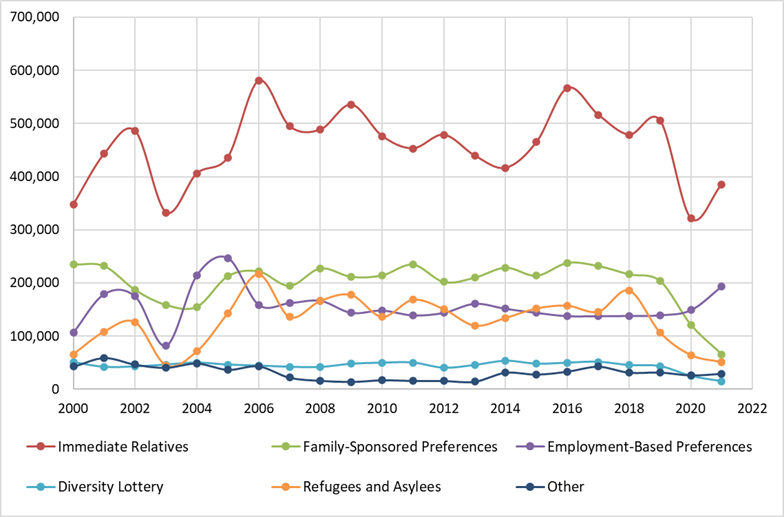

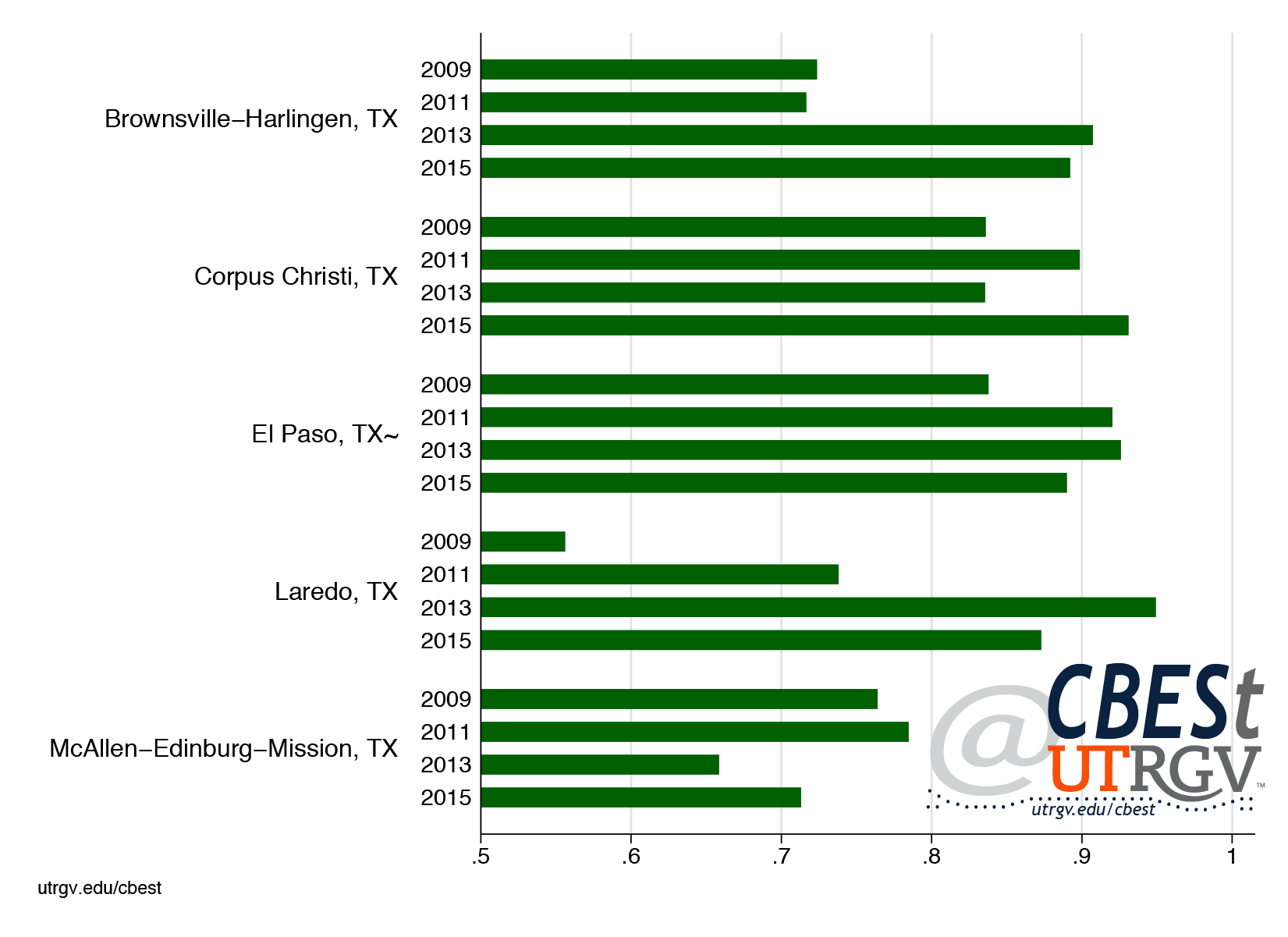

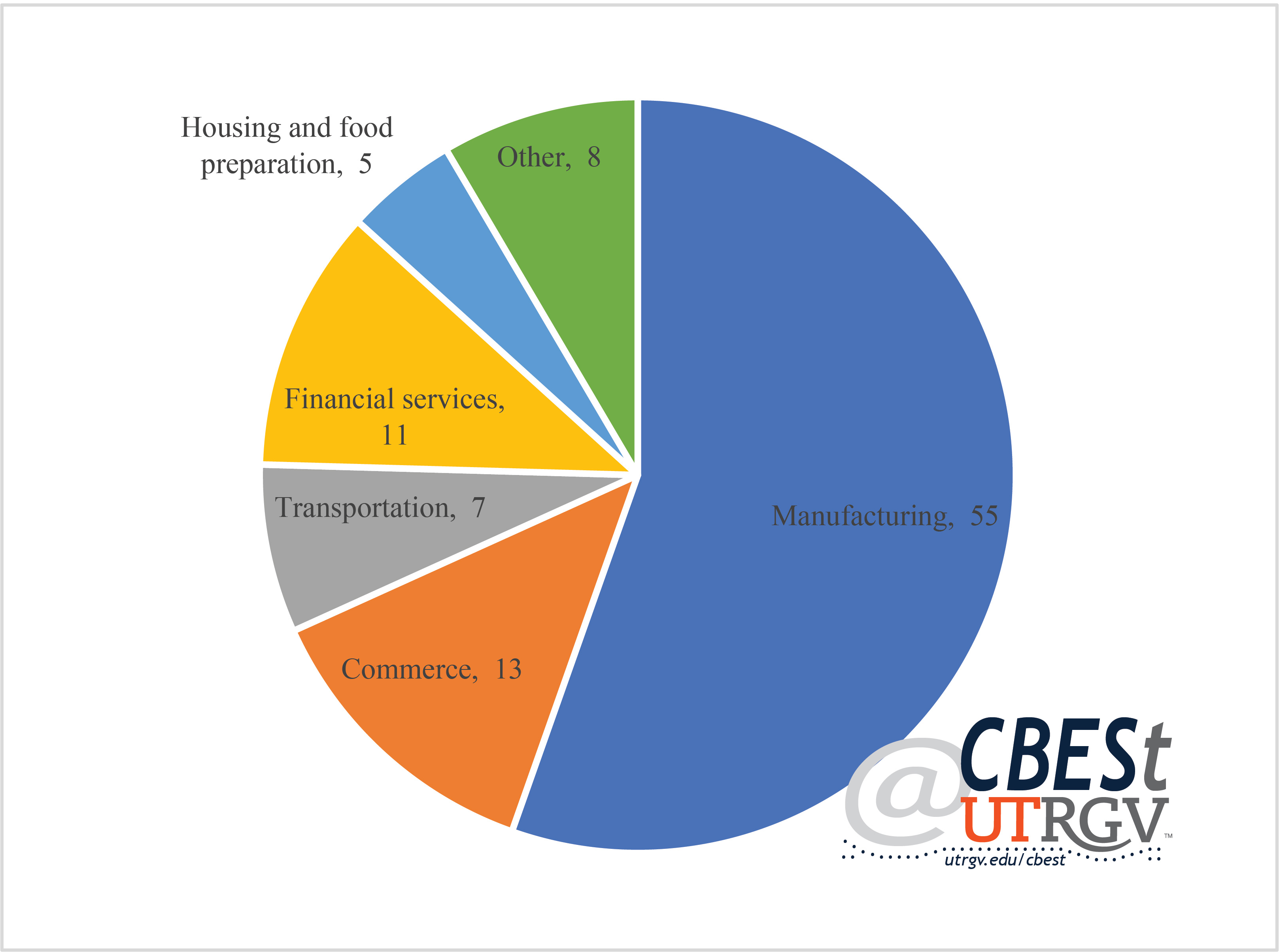

The number of permanent resident permits given in the US for the period 2000-2021 are shown in figure 1. For the years 2000-2019, which do not include the last 2 years as they can be atypical due to the pandemic, approximately 65% of all the permanent residence permits were allocated towards family-based immigration, which represents an average of about 680,000 permits per year. Skill-based categories represent about 154,000 permits per year (almost 15%), refugees and asylees were given an average of 135,000 permits (almost 13%) while about 47,000 (4.5%) permits were allocated to the diversity lottery. Finally, about 3% were given for other categories.

Source: Department of Homeland Security, Yearbook of Immigration Statistics. Various years. Available at https://www.dhs.gov/immigration-statistics/yearbook

For people that do not have close relatives which are US citizens nor qualify for having special skills that would allow them to migrate to the US (e.g. a Ph.D. from an American University), there does not exist a mechanism that would allow them to come to the US to work legally either in a temporary or permanent way. For those individuals, the only way to come and work in the US is via unauthorized immigration, either in the form of crossing the border illegally (mostly through the Mexican border) and which is a very risky proposition that often involves paying large sums to human smugglers better known as “coyotes” as well as a very dangerous journey, or in the case of having a temporary visiting permit (i.e. a tourist-visa) by violating the terms of their stay (typically overstaying in order to work).

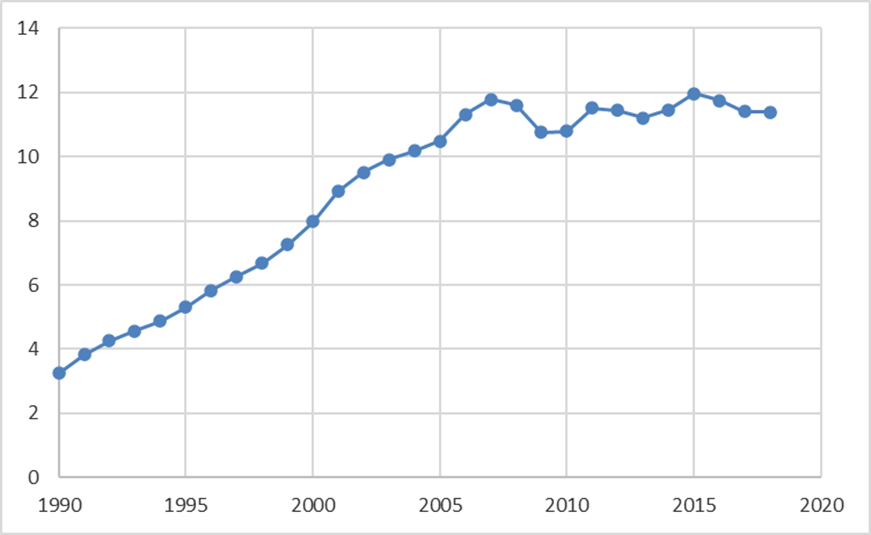

Figure 2 displays the stock of unauthorized immigrants for the period 1990-2018. This number starts at about 3 millions in 1990, and reaches a maximum of 12 millions in 2007 and 2015, with a decrease in 2008-2010 due to the effects of the housing crisis which dried up the demand for many jobs which unauthorized immigrants tend to occupy (e.g. construction workers) as well as the effects of the economic downturn. These numbers are in the aftermath of the legalization (amnesty) of 2.7 millions of unauthorized immigrants under the Immigration Reform and Control Act (IRCA) passed in 1986. IRCA also devoted more resources for border enforcement in an attempt to control future unauthorized immigration.

Source: Department of Homeland Security at https://www.dhs.gov/immigration-statistics/population-estimates/unauthorized-resident from 2005 to 2018. Years 1990 to 2004 inferred from growth rates constructed from estimates of the unauthorized population residing in the US by Warren and Warren (2013).

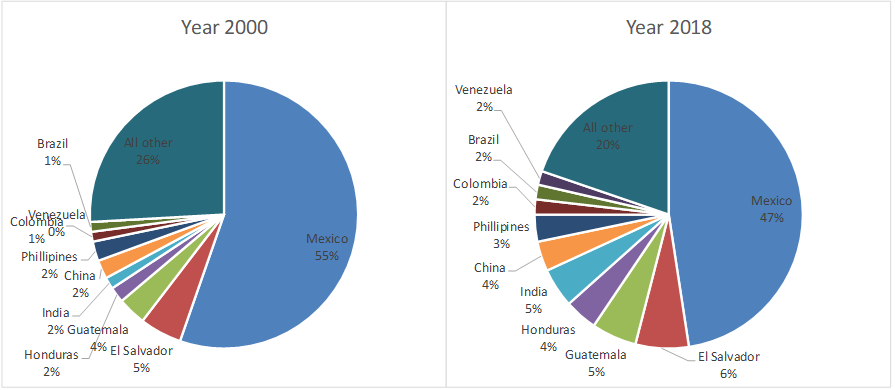

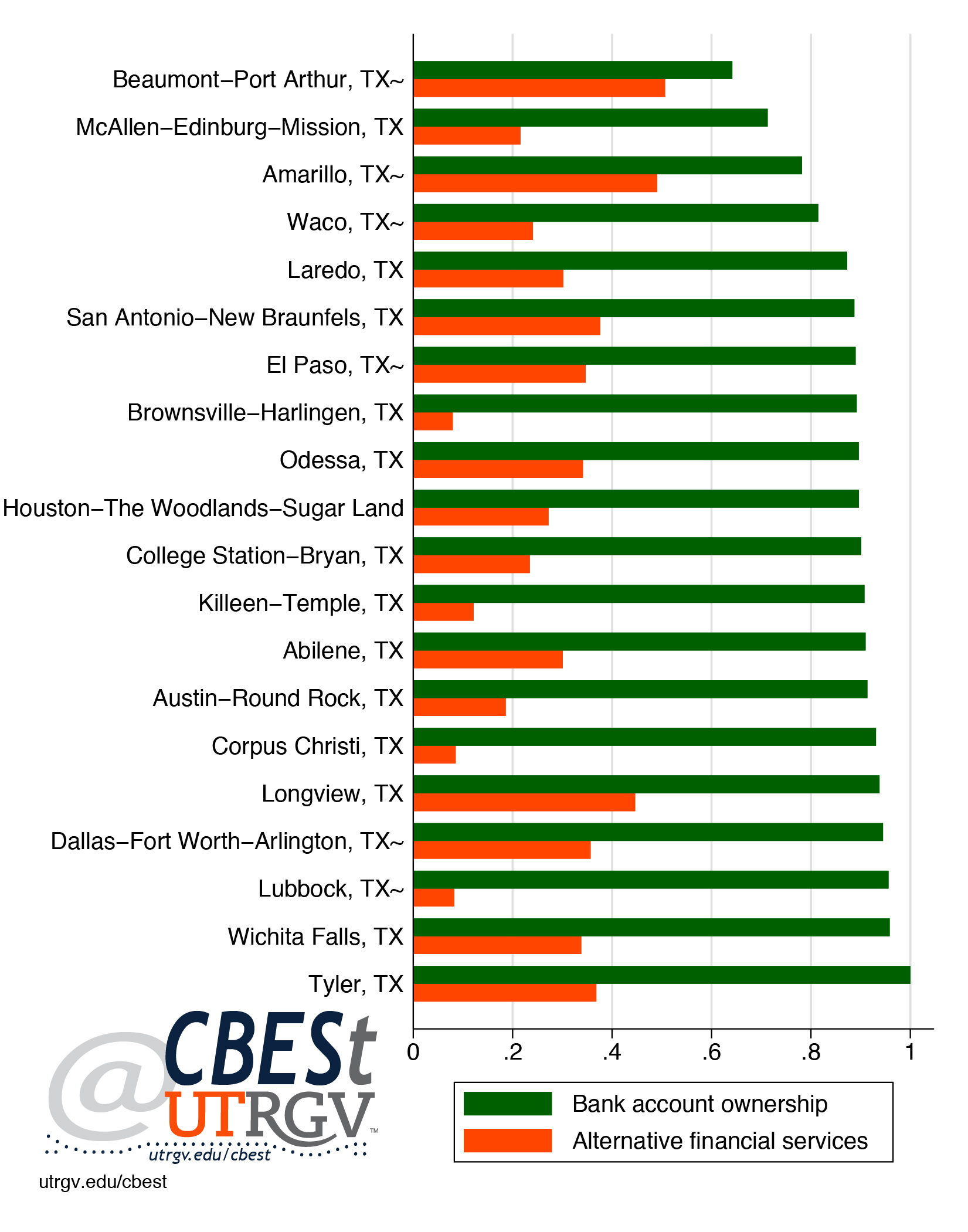

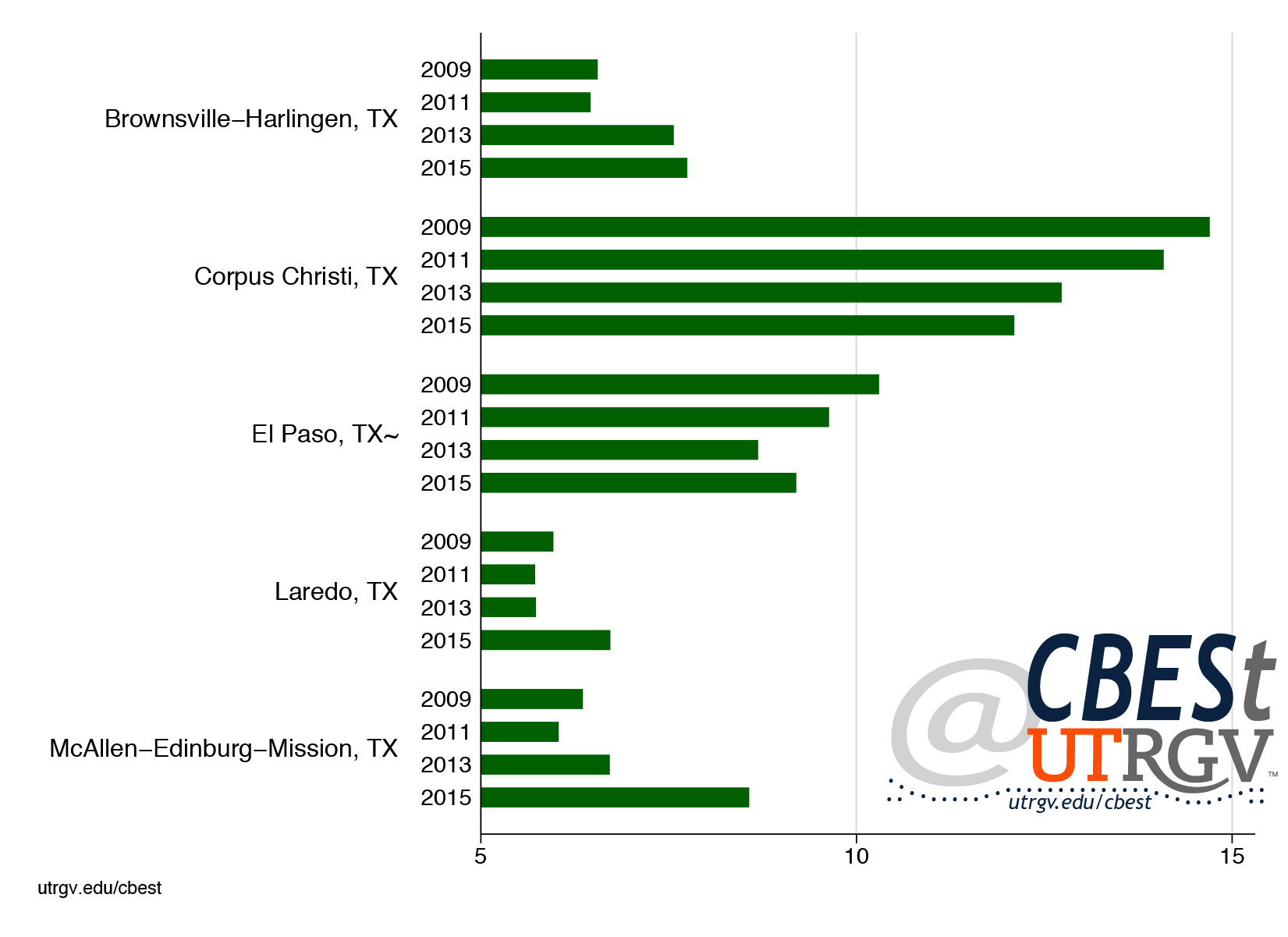

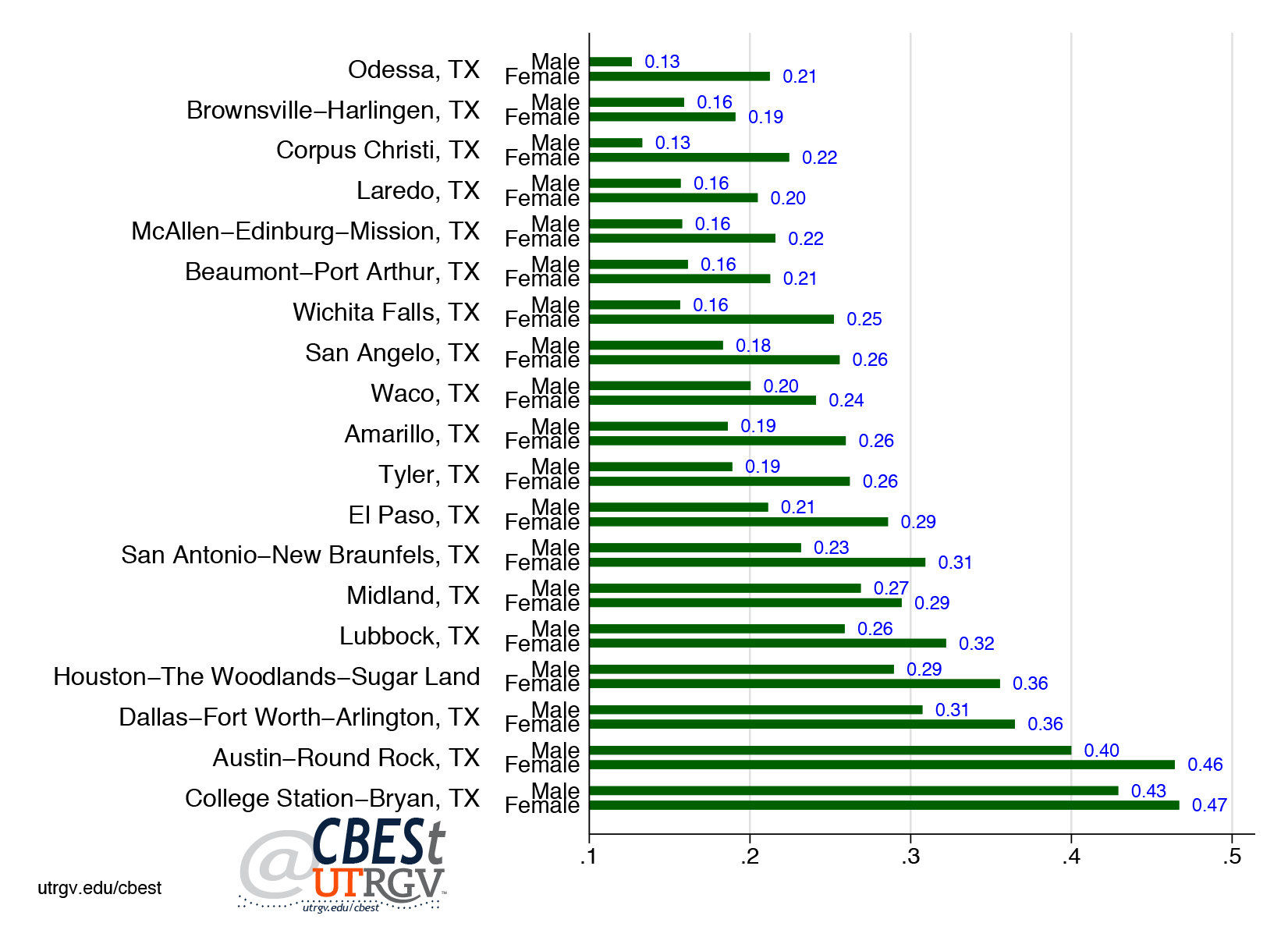

With regards to whom specifically are these unauthorized immigrants, figure 3 shows two snapshots of their country of origin for years 2000 and 2018. Mexican citizens represent the largest share, but such number has (steadily) decreased from 55% in 2000 to 47% in 2018. Central American countries have seen their shares increased over the same period: El Salvador from 5% to 6.4%, Guatemala from 3.4% to 5.4% and Honduras from 2% to 4%. At the same time, there are other countries who used to represent a small share of unauthorized immigrants but who now make a significant amount: China, India and Philippines accounted for about 6% of the total stock of unauthorized immigrants in 2000 but accounted for almost 12% in 2018 (most of their citizens via overstaying their visas rather than crossing the border without a visa). Similarly, Venezuela, Colombia and Brazil used to represent about 2% in 2000 but represent slightly more than 5% in 2018.

Source: Department of Homeland Security, Estimates of the Unauthorized Immigrant Population Residing in the United States available at https://www.dhs.gov/immigration-statistics/population-estimates/unauthorized-resident

Flows of unauthorized immigrants respond to “pull” (from the host economy) and “push” (from their country of origin) factors, as well as to the level of enforcement in the host country (see for example Orrenius and Zavodny (2013) and the references therein). High growth and low unemployment in the host economy are factors that tend to attract immigrants, while low growth in the sending economies, high unemployment and political instability in the sending economies are factors that tend to increase the supply of immigrants, everything else constant. For these reasons, the flow of unauthorized immigration is to be thought of as “equilibrium” migration flows which adjust in response to these forces.

In the case of family-based migration flows, since the US laws are such that there is no limit to who can come in the form of immediate relatives (parents, natives and children of American citizens), it implies that they are also equilibrium migration flows. Skill-based immigrants may or may not be an equilibrium flow in the sense that there is a limit in the number of high-skilled immigrants that can come to the US in a given year and that number is typically exhausted every year (thus the short side of the market would determine skill-based immigrants flows), while the case of refugees is a category that the US decides for diplomatic reasons in response to conflicts and international crisis/disasters.

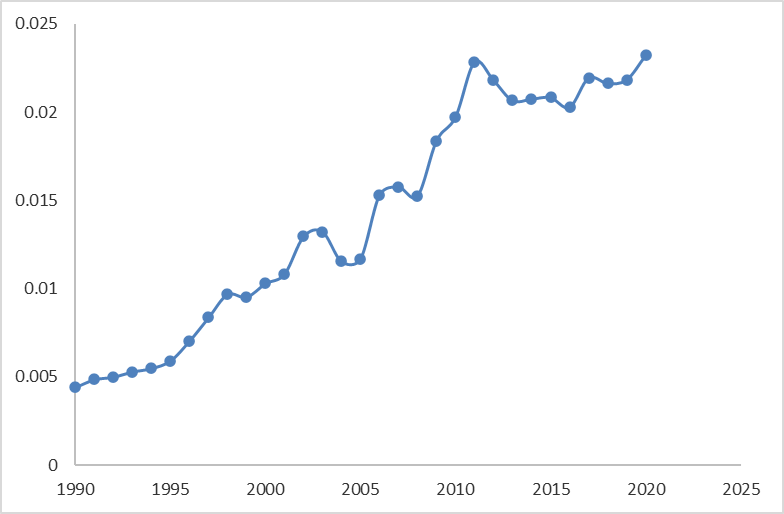

Source: US GDP: World Development Indicators, series NY.GDP.MKTP.CD at https://databank.worldbank.org/source/world-development-indicators#. Data on Budget of the Border Patrol from American Immigration Council, available at https://www.americanimmigrationcouncil.org/research/the-cost-of-immigration-enforcement-and-border-security.

Figure 4 illustrates that expenditure in enforcement, as captured by the US Border Patrol budget for the period 1990-2021, has been steadily increasing from almost .005% of GDP in 1990 to almost .023% of GDP in 2021. Yet unauthorized immigration kept increasing for much of this period until the housing crisis hit in 2008. Precisely because unauthorized migration responds to different forces, for all practical purposes bringing unauthorized immigration to 0 is impossible to achieve as there are real costs of enforcing the border and there are other variables that enter the decision whether to migrate or not in an unauthorized way, in addition to moral issues and diplomatic relations.

A possible amnesty for unauthorized immigrants has cost and benefits that are hard to quantify. Among the benefits, one can expect higher rates of income taxes paid by immigrants (though many do pay income taxes via an ITIN number[1]) from having a legal status; better allocation of talent as currently those immigrants tend to concentrate in certain industries for which a job doesn't require a social security number (e.g. construction workers, gardeners, domestic workers, etc.) as opposed to working in the sector where their productivity is highest and which would also lead to higher tax revenue; and there's also the human benefit that there are many families in the US where some of the members have legal status but some others do not. On the cost side, unauthorized immigrants do not qualify for most government transfers and so any amnesty would likely impact those costs. Similarly, unauthorized immigrants currently do not have social security benefits (even though some of them do pay social security taxes by means of an ITIN number) which could change under a possible amnesty. Also, as Orrenius and Zavodny (2013) have argued, IRCA lead to more legal immigration since the current system favors family-reunification. So, after gaining legal status, many of the legalized immigrants through IRCA were able to petition for their relatives once they became US citizens. Another point of contention is the right to vote that immigrants might obtain if they choose to become citizens (typically after having at least 5 years of permanent residence). Finally, there's an expectation channel where a current amnesty could lead to an expectation of a future amnesty as this arguably happened with IRCA, and hence in the absence of other enforcement measures and some form of temporary/guest worker program (discussed later), continued unauthorized immigration could be the result. Hence the political hot-potato that is any possible amnesty.

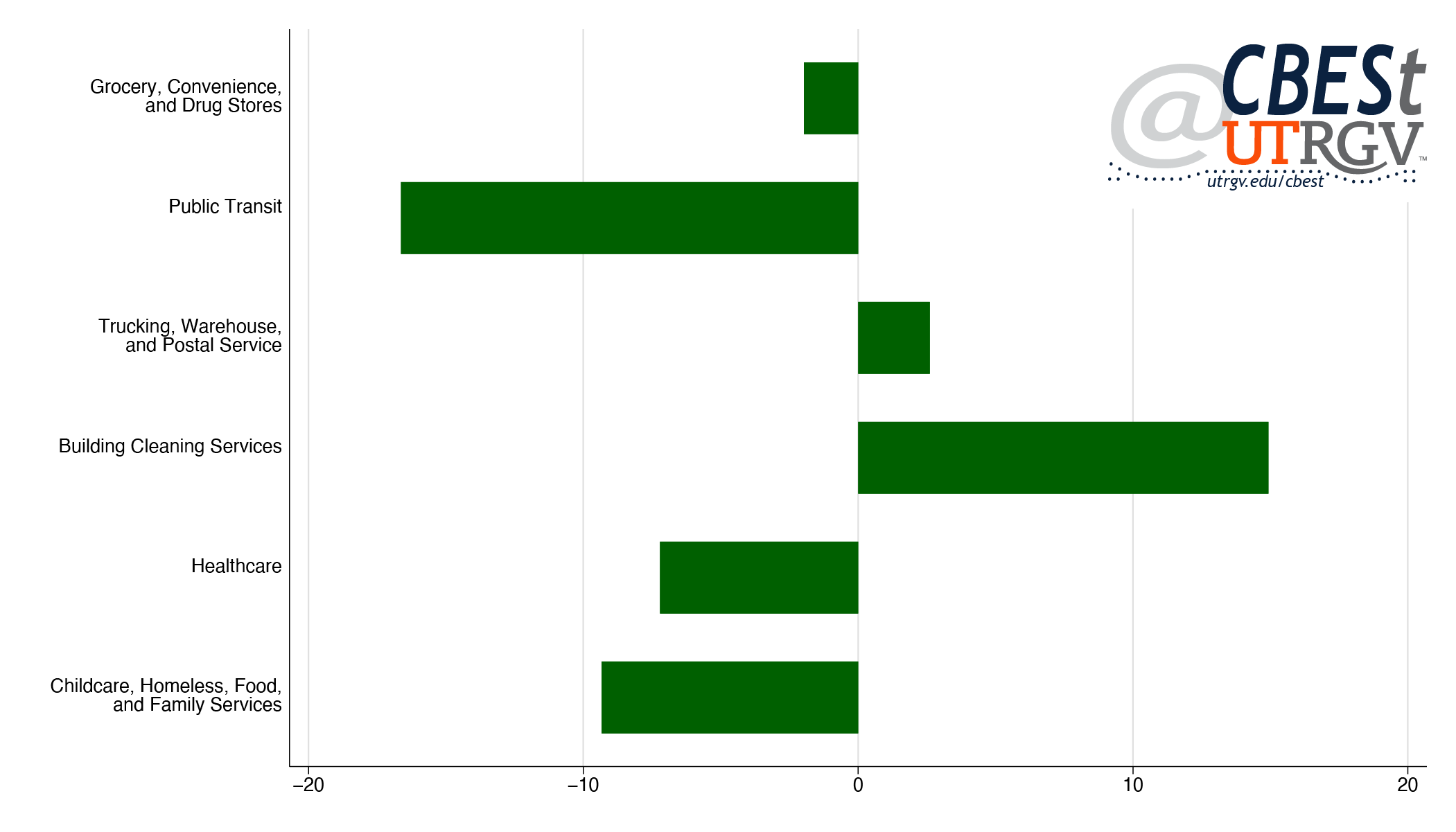

Arrest Data

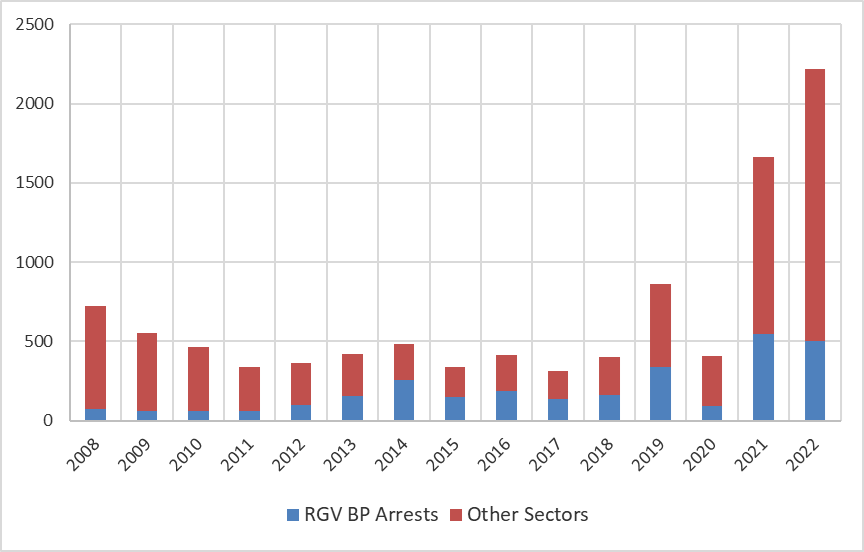

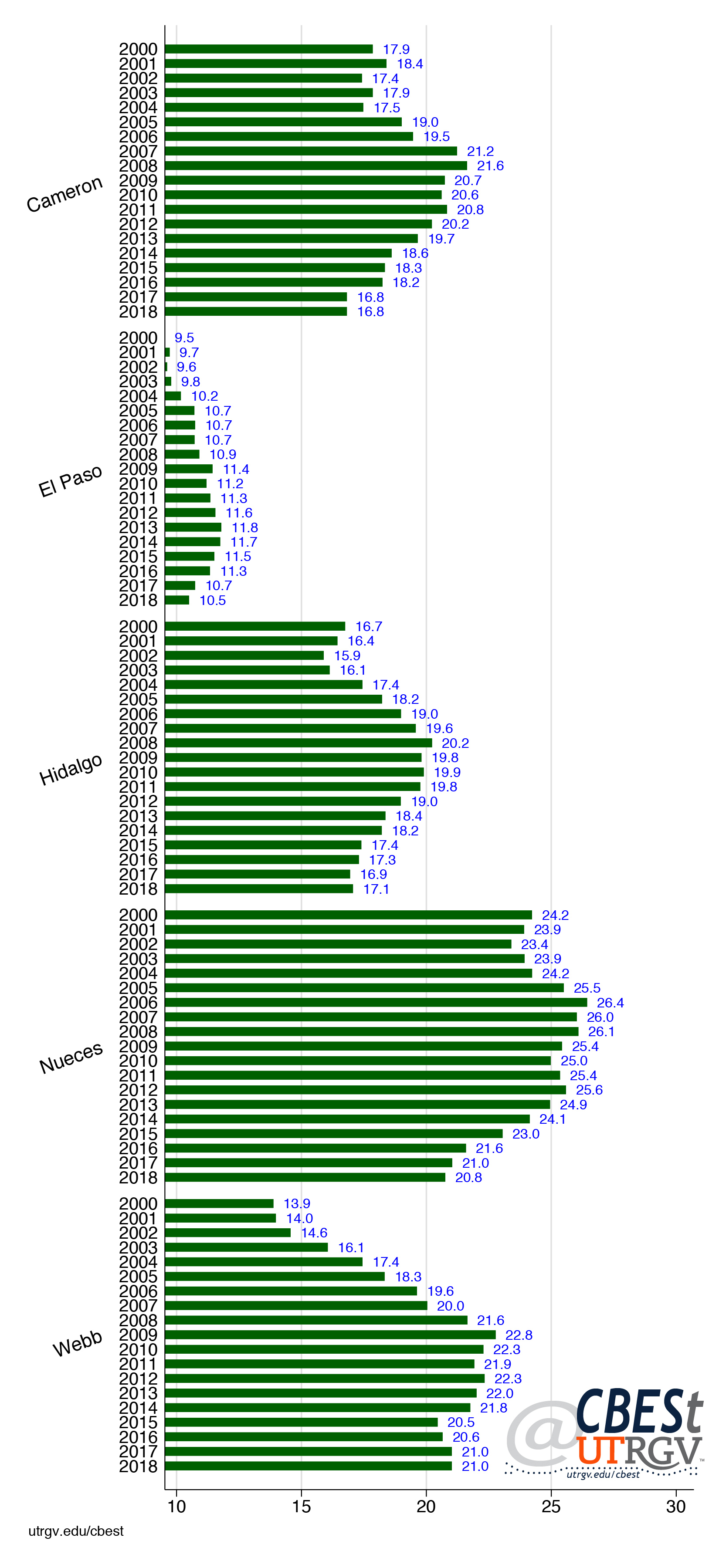

Arrest data offers an interesting snapshot of who comes to the US in an unauthorized way. Figure 5 shows the number of arrests by the border patrol along the Mexican border, starting in 2008 as available from the Transactional Records Access Clearinghouse (TRAC) at Syracuse University. Starting in 2008, these numbers stayed below 500,000 arrests per year until 2019 which saw 860,000 arrests, then decreased during 2020 when countries closed borders and much of the economic activity was restricted during the early stages of the COVID pandemic. Finally, 2021 and 2022 have seen these numbers skyrocket to 1.65 and 2.2 million arrests respectively.[2]

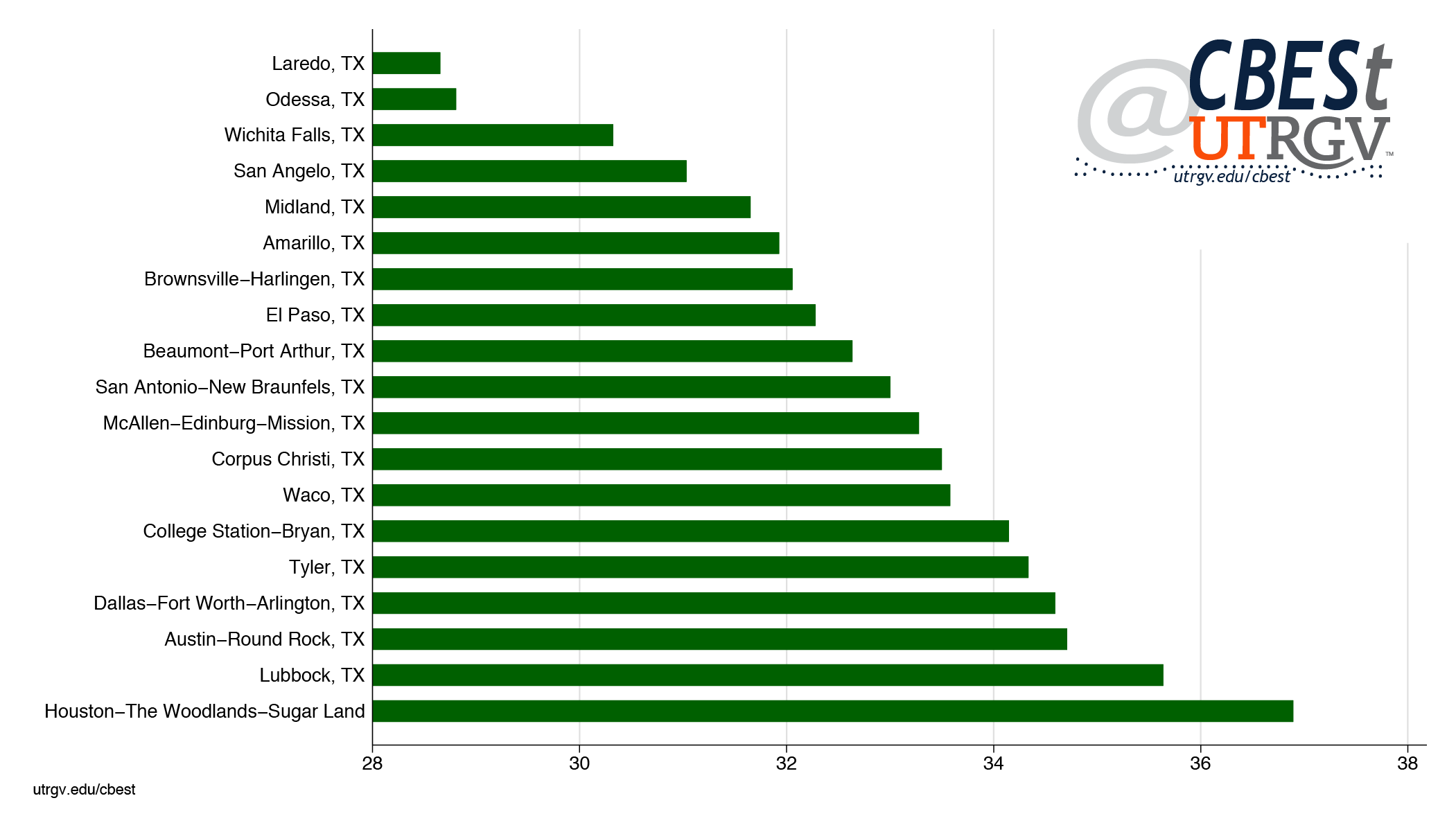

The border Patrol divides the border with Mexico into 9 sectors. Five of these are located in Texas, which are Rio Grande Valley (RGV), Laredo, Del Rio, Big Bend and El Paso sectors. The other sectors covering the border with Mexico are Tucson, Yuma, El Centro and San Diego. Figure 5 also shows how many of the annual arrests took place in the RGV Sector.

From 2008 to 2011 The RGV sector had between 10 and 20% of all the arrests in the Mexican border. Starting in 2012 the RGV has become the sector with the most arrests, suggesting that there are more attempts to cross through this sector. Indeed, more than 52% of all the arrests during 2014 took place in the RGV. More recently, in 2021 the RGV share of arrests was 33%, which corresponds to about 549,000 arrests in 2021.[3]

Source: Transactional Records Access Clearinghouse (TRAC) at Syracuse University, available at https://trac.syr.edu/phptools/immigration/cbparrest/ . Total arrests for year 2022 available at https://www.cbp.gov/newsroom/stats/cbp-enforcement-statistics . Number of arrests at Rio Grande Valley sector for year 2022 are a projection from the observed numbers from TRAC for 2022 arrest numbers until July of 2022.

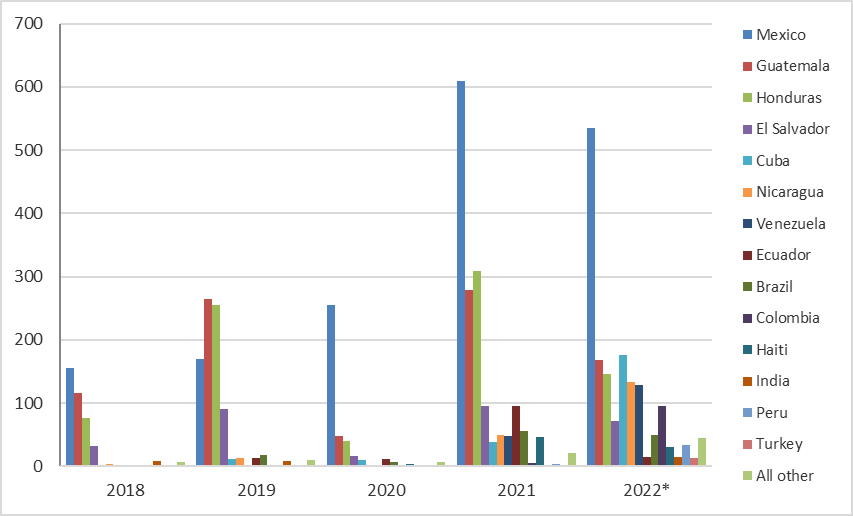

Figure 6 shows the countries of origin of the people most recently arrested by Border Patrol Officers, starting in 2018. In previous years, most of these unauthorized immigrants used to come from Mexico, Guatemala, Honduras and El Salvador. Starting in 2021, a significant share of those arrests corresponds to individuals from other countries. In particular, other Central and South American countries including Cuba, Nicaragua, Venezuela, Ecuador, Brazil, Colombia, Haiti and Peru represented less than 2% of the arrests in 2018 when combined (and also in previous years, not shown), but lately those countries represent 20% of the arrests in 2021 and 40% of the arrests in 2022 (with data until July of 2022). There are also distant countries that historically were not represented among the arrested at the southern border, including people from India (14,826 arrests from January to July of 2022), Turkey (12,562), Romania (5,455), Georgia (4,728), Russia (3,987), Uzbekistan (2,755), Senegal (2,237), Bangladesh (1,790), Ghana (1,751), Angola (1,455) and China (1,244), among many others.

At this level of generality and without more data it is impossible to disentangle the specific reasons for why the recent increase in arrests and which presumably implies both a higher number of people arrested (as there is a possibility of attempting to cross multiple times) and a larger pool of people attempting to cross in an unauthorized way (some of which are successful and of course do not get counted in arrest data), but a few reasons are easy to identify. First, the pandemic affected countries in unexpected and asymmetric ways (not all sectors were equally affected) and thus lack of opportunities in the sending countries might have precipitated at least some of this increase. Second, the timing is also consistent with the change of administration in the US. There might be a perception by immigrants that the Biden administration might be less inclined to expel immigrants as compared to the Trump administration (though the Biden administration kept using title 42 to quickly expel immigrants attempting to obtain asylum in the US until May 11th of 2023).[4] The evidence from both old countries and the newer countries comprising a significant number of arrests at the southern border also suggest either an expectations channel, or perhaps diffusion of know-how about how foreigners can come through Mexico in order to attempt to cross into the US.

Source: Transactional Records Access Clearinghouse at Syracuse University, available at https://trac.syr.edu/phptools/immigration/cbparrest/ . Data for 2022 until end of July.

Finally, title 42 which started in March of 2020, resulted in many people sent to Mexico during the pandemic, and this in turn created incentives to repeatedly attempting to cross into the US. Hence it is possible that the numbers for 2021 and 2022 are much more inflated than previous years in terms of counting aliens attempting to cross (as opposed to counting number of arrests). It is possible to estimate the number of aliens apprehended from the data on repeated arrests, which yields an estimate of slightly more than 1 million of aliens arrested in 2021, a number still higher than the number of arrests (also overstating aliens arrested but probably less) in any previous year to 2021 and thus the increase in foreigners remains.[5]

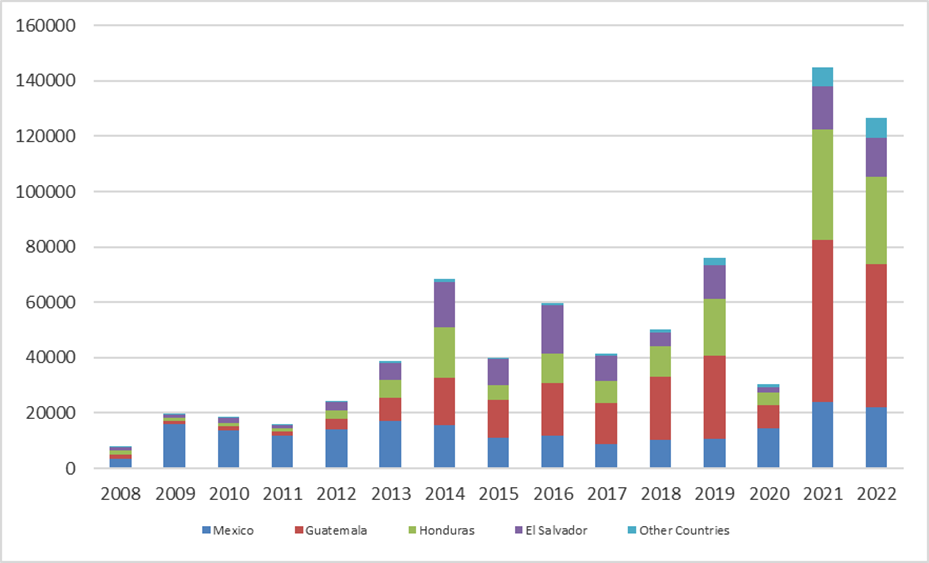

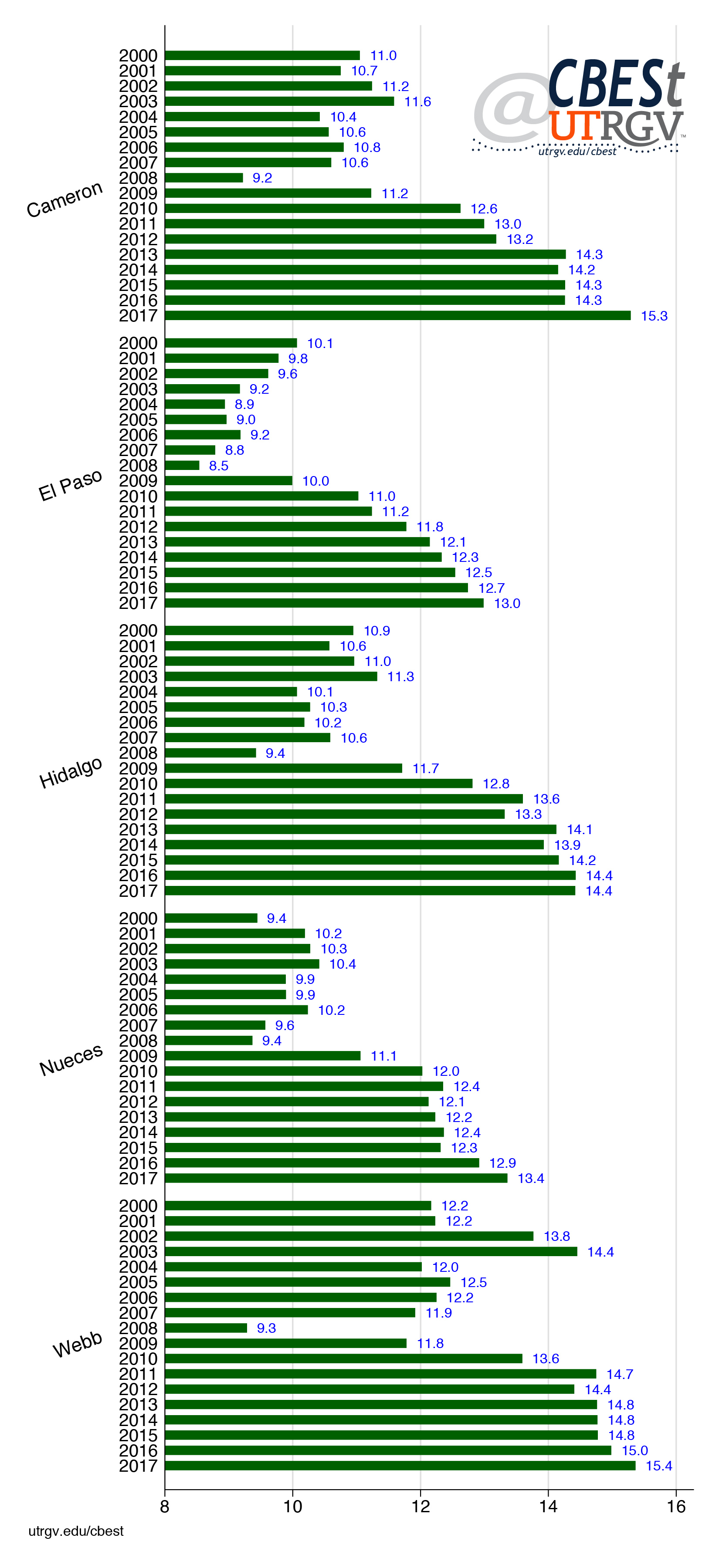

Figure 7 shows another recent phenomenon, the rise in the number of unaccompanied children coming to the US. In 2008 the total number of unaccompanied children was slightly above 8000, while in 2021 this number was almost 145,000. During the period discussed, more than 95% of them came from Mexico, Guatemala, Honduras, and El Salvador and for most of the period there was an upward trend. Recently (2021) the biggest shares came from Guatemala (40%) and Honduras (27%).

But why the increase in unaccompanied children? The situation of the sending economies could help explain some of these flows as the countries in Central America are relatively poor compared to other countries in the American continent, with a high poverty rate and violence. Then there is also incentives. In 2008 the US passed the William Wilberforce Trafficking Victims Reauthorization Act of 2008, which among other things created specific legal protections for minors traveling alone and which can produce a tension between the objectives of protecting the children from trafficking and the improved incentives for minor migrants to come unaccompanied precisely because of the better protection and possibility of staying at the US while their case is resolved.

Source: Transactional Records Access Clearinghouse at Syracuse University, available at https://trac.syr.edu/phptools/immigration/cbparrest/ . Data for 2022 until end of July.

Since 2012, the majority of unaccompanied children have been arrested at the border through the RGV sector. For example, in 2021 in the RGV sector there were 76,284 arrests out of 144,873 minors arrested (almost 53%).

Often, minors turn themselves at the border to be arrested, as they are typically held in detention, and finally released to some family member in the US or to some sponsor after some days (perhaps months when detention centers are full). Of the minors which have been apprehended from 2014 to 2019, only 4% have been expelled (Hesson and Rosenberg (2021)). In addition, under title 42 (discussed below) during the pandemic minors could be expelled if traveling with their families, but not necessarily if they were traveling alone and which reinforces the incentive to split at the border -assuming they have someone on the US waiting for them. Finally, these numbers cannot show how many minors are abused, exploited and even die during the journey from other countries as only those that arrive and are arrested are counted.

Concluding Remarks

There are different types of immigrants and many different programs in the US that regulate immigration (directly in the case of legal immigration and indirectly via enforcement in the case of unauthorized immigration). This note attempts to present the state of immigration flows to the US and discusses some of the immigration challenges. Due to the complexity of the topic and in order to keep the discussion short, the note does not attempt to discuss comprehensive immigration reform.[6]

With respect to unauthorized immigration, addressing push factors (violence, lack of opportunities, poverty, etc.) is clearly important but it is something that depends heavily on the institutions and quality of the government of the sending countries. What a host economy like the US can control is the level of legal migration allowed into the country as well as the type and level of enforcement. An enforcement-only approach is unlikely to control unauthorized flows and is also likely to impose high human costs. There is possibly a better solution that could represent a win-win situation for the US and to many would-be unauthorized immigrants: the possibility of a guest or temporary worker program.

There are some advantages of a guest worker program when the alternative is unauthorized immigration[7]: it would allow for a way to come and work for a category of people that currently have no legal way of coming to the US. The stay is temporary as opposed to permanent as the current system ends up inducing unauthorized migration with a long stay (see Orrenius and Zavodny (2013)) due to the high costs of crossing.[8] Since by definition a guest worker program allows people only temporary in US soil, in a decade there could be a larger number of people who would benefit from working in the US temporarily as opposed to the same stock of people over many years under unauthorized immigration. Then those temporary workers would return to their home economies with some capital. Also, for national security issues, a guest worker program would be preferred over unauthorized immigration. Finally, other countries that are traveled during the journey to the US (e.g. Mexico) would also benefit from the existence of such program as many of the immigrants that are rejected in the US might end up in Mexican cities.

Some of the big winners of the status-quo are the criminal groups which charge significant amounts of money in attempts to smuggle people into the US or who kidnap or exploit foreigners while in transit to the border. Because of that, many potential immigrants would prefer to apply for a legal temporary worker permit, thus leading to some tax revenue (cost of the permit) plus some savings as compared to an enforcement-only framework in that the pool of potential unauthorized immigrants would be theoretically lower. Finally, the journey to come to the US would not be as dangerous as it is right now.

____

Armando R. Lopez-Velasco is an Assistant Professor of Economics at The University of Texas Rio Grande Valley.

Endnotes

- American Immigration Council, “How the United States Immigration System Works”, retrieved on 5/26/23. Available at https://www.americanimmigrationcouncil.org/research/how-united-states-immigration-system-works

- Kerr, Sari Pekkala & William R. Kerr (2011), “Economic Impacts of Immigration: A Survey”. NBER Working paper 16736, National Bureau of Economic Research Inc.

- Lopez-Velasco, Armando R. (2022), “On the Design of an Optimal Immigration Policy”. Available at SSRN: https://ssrn.com/abstract=4047652 or http://dx.doi.org/10.2139/ssrn.4047652

- Orrenius, Pia M. and Zavodny, Madeline (2012). "The Economic Consequences of Amnesty for Unauthorized Immigrants," Cato Journal, Cato Institute, vol. 32(1), pages 85-106, Winter.

- Transactional Records Access Clearinghouse at Syracuse University, available at https://trac.syr.edu/phptools/immigration/cbparrest/

- United States. Department of Homeland Security (2021). Yearbook of Immigration Statistics. Washington, D.C,: U.S. Department of Homeland Security, Office of Immigration Statistics, 2022.

Footnotes

Fall 2022 v18, n2

Taming Inflation: The Tradeoffs of Monetary Tightening

Maroula Khraiche and Andre Mollick

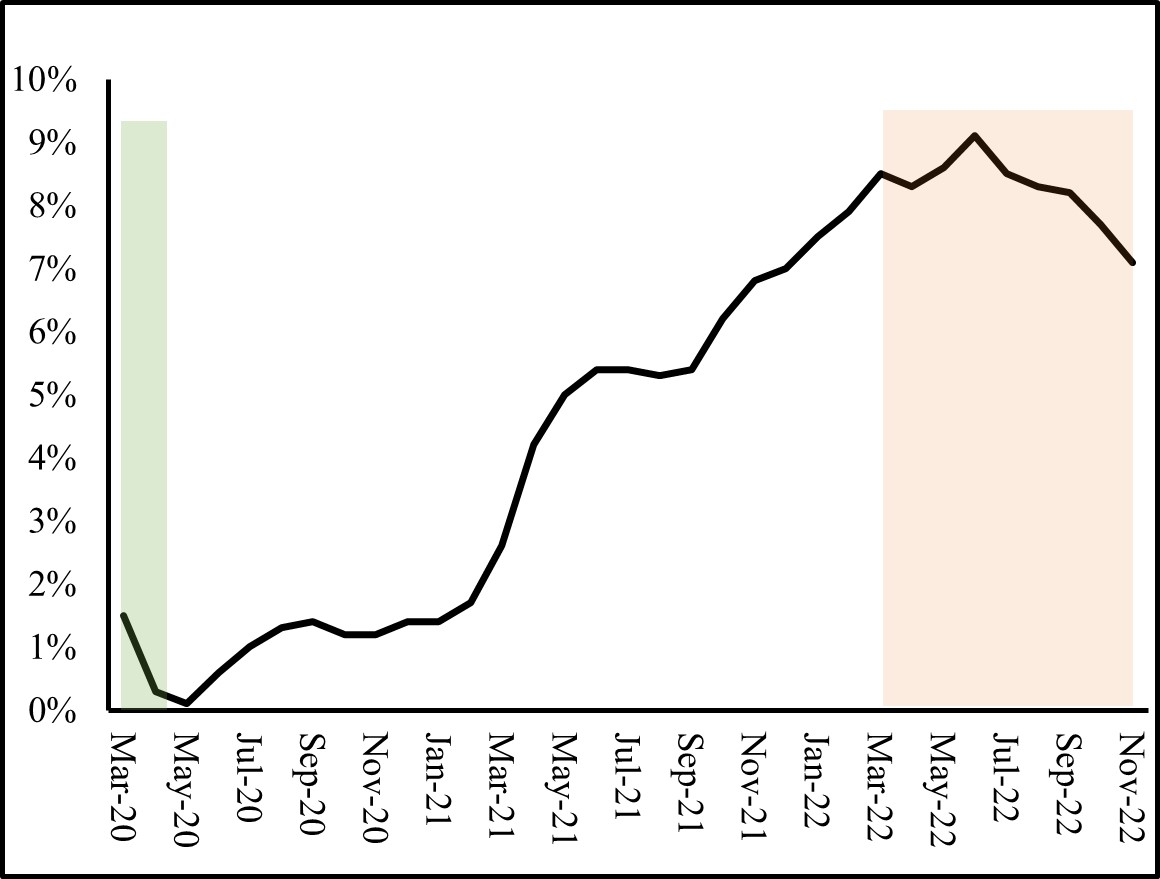

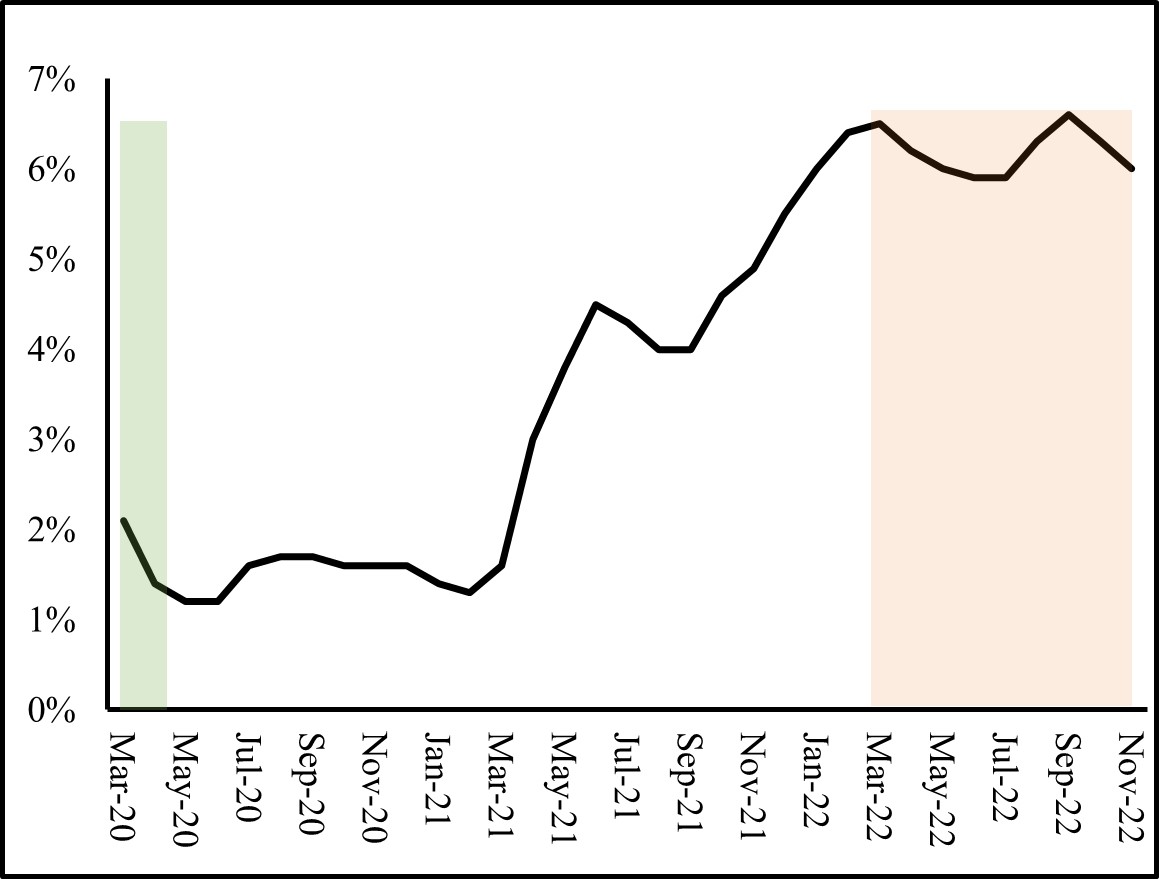

In the summer of 2022, consumers experienced the highest inflation rates in decades. In June of 2022, the Consumer Price Index (CPI), rose 1.3% compared to May, which implied a 9.1% increase over the past 12 months. The CPI is a measure of the average change over time in the prices paid by consumers for a basket of goods, therefore, changes in the CPI pin down inflation faced by consumers. In more welcome news released on December 12th, 2022, the U.S. Bureau of Labor Statistics (BLS) reported that the CPI rose only by 0.1% in November compared to the previous month. This implies that over the last 12 months, inflation was 7.1% . Nonetheless, this level of inflation is still higher that the 2% historically targeted by central banks. If fact, economists view such a high inflation rate as destabilizing. Panel (a) in Figure 1 depicts the fall and then sharp increase in the growth rate of the CPI (i.e., inflation) since the beginning of the pandemic until November of this year.

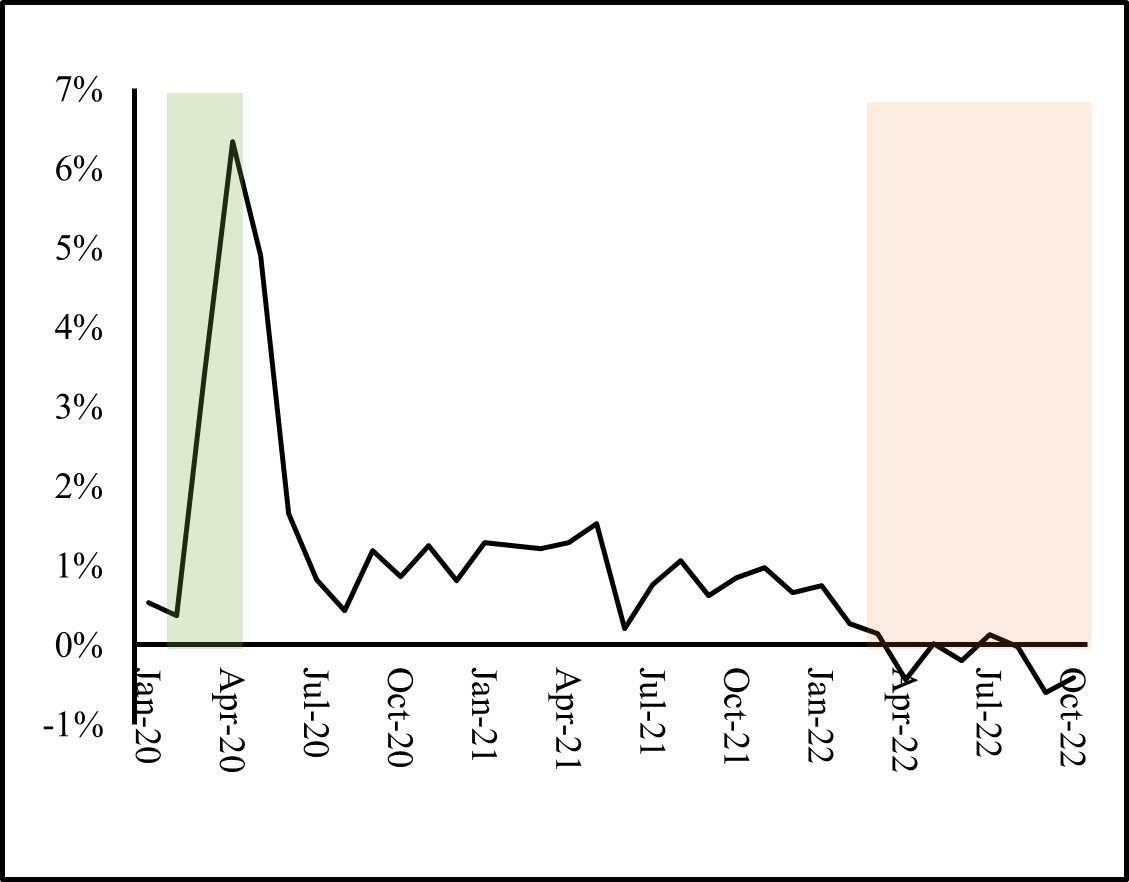

Another worrying sign is that inflation has exhibited a persistent upward trend over the past year. Initially, these inflationary pressures were thought to be transitory resulting from the imbalance between supply and demand created by the pandemic; elevated demand partially driven by extra funds households received from relief packages was met with shortages and supply chain interruptions. Furthermore, Russia’s invasion of Ukraine raised food and energy prices, which raised costs and added to the price pressures. Yet looking at the core inflation rate, which excludes food and energy prices, high and persistent trends in inflation are still detected. Over the past year, core inflation grew about 6.5% in the U.S. pointing to causes other than the rise in energy prices. Panel (b) in Figure 1 shows the increase in core inflation. With the economy still recovering from the pandemic and in hopes that the rise in prices would resolve as supply chain disruptions and pandemic fueled demand for goods dissipated, the Federal Reserve (Fed) was slow to respond, further fueling inflation. What’s causing this persistence in inflation? One explanation is the public’s expectations. Inflation tends to have momentum and as people expect higher prices, higher prices materialize. However, another predictor of future inflation is the growth of money. Money supply rose dramatically over the past two years as the Fed cut interest rates to near zero to stabilize the economy during the pandemic. Panel (a) in Figure 2 shows the steep rise in money supply measured as M2. According to the St. Louis Fed, as of May 2020, M2 consists of M1 plus small-denomination time deposits and balances in retail MMFs and M1 consists of currency, demand deposits at commercial banks and other liquid deposits, consisting of OCDs and savings deposits (including money market deposit accounts).

This report discusses the role policy may have played in fueling inflation and the role it is playing in taming it. Despite the focus on policy in this report, it is worth noting that the extraordinary economic shock of the pandemic has also had an effect on aggregate price and this effect has yet to fully disappear and may be even more important than policy.

Figure 1: The Consumer Price Index for All Urban Consumers, Annual Percent Change

Green area indicates the Covid recession, orange area indicates the period of monetary tightening. Source: Bureau of Labor Statistics

(a) All Items

(b) All items less food and energy

Fiscal and Monetary Response

During the pandemic, both fiscal and monetary policy were used extensively to keep the economy afloat during this extrordinary health crisis. Fiscal policy is defined as the use of government revenue and spending in order to influence the economy. During the pandemic, expansionary fiscal policy amounted to $5 Trillion in stimulus and relief packages. The Coronavirus Preparedness and Response Supplemental Appropriations Act which passed in March, 2020, allocated $8.3 billion to state and local governments to fight the spread of the virus, fund research for a vaccine, and support efforts to stop the spread of the virus overseas. Families First Coronavirus Response Act (FFCRA) was also passed. FFCRA allocated $192 billion to help families who rely on free school lunches, aid small firms finance paid sick leave for those suffering from COVID-19, add $1 billion to unemployment insurance in states, and fund COVID-19 testing [1]. During the same period, the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) allocated $2.2 trillion to help families and industries, established the Paycheck Protection Program (PPP) and the Economic Injury Disaster Loan (EIDL) and contained additional funding for hospitals and COVID-19 testing [3]. In 2021, the Consolidated Appropriations Act allocated $900 billion (some of which was distributed as direct payments to households) and the American Rescue Plan paid out $1.9 trillion in various relief for firms and households [5].

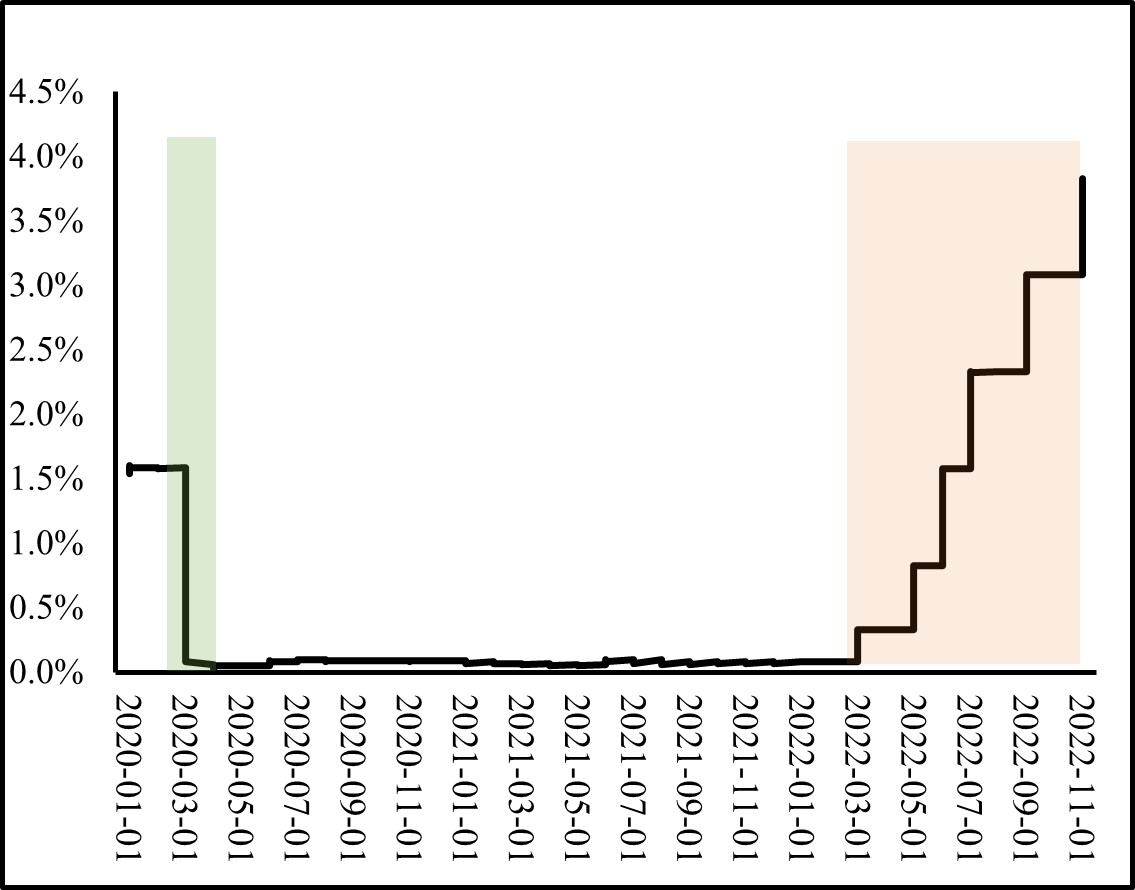

Monetary policy is undertaken by the Federal Reserve (the United States’ central bank) which generally adjusts money supply and interest rates in order to achieve economic goals. During the pandemic, providing liquidity and ensuring the stability of the financial system and the economy were the focus of the Fed. Therefore, the Fed cut the Federal funds (FF) rate by 1.5 percentage points on March 3 and March 15, 2020. These cuts lowered the short-term FF rate to a range of 0% to 0.25% (see panel (b) of Figure 2). In doing so, the Fed reduced the costs of borrowing and freed up reserves for banks, ensuring ample liquidity when needed and encouraging banks to make loans. Cutting the interest rates is typically achieved by increasing money supply through bond purchases (see box below), therefore, money supply rose dramatically in 2020 and 2021.

Another policy tool that the Fed has been employing since the Great Recession of 2007-2009 is Quantitative Easing (QE). At the time, cutting the FF rates to almost zero was not sufficient to spur on economic recovery. As a result, the Fed employed QE which involves the purchases of Treasury securities and mortgage-backed securities (MBS) using newly created electronic cash. Such purchases by the Fed boost banks’ reserves and lowers long term interest rates. On March 15, 2020, the Fed resumed the purchasing of large amounts of Treasuries and residential and commercial MBS initially to stabilize markets and then continued on with QE to provide further liquidity to markets [6]. In December of 2020, the Fed indicated that it would slow these purchases tapering its purchases further in December 2021.

Figure 2: Money Supply and Target Interest Rates

Green area indicates the Covid recession, orange area indicates the period of monetary tightening.

Source: St. Louis Fed

(a) Monthly M2, Monthly Percent Change

(b) Daily Effective FF Rate, Percent

FOMC and FF rate: The federal funds rate is a short-term interest rate at which banks trade the balances they have at Federal Reserve Banks with each other. Although the effective federal funds rate is determined in the market as banks with more liquidity negotiate lending rates with those seeking liquidity, this rate is also influenced by the Federal Reserve. If the Fed wishes to reduce the rate, the Fed instructs its traders to buy short term government bonds from banks, which in turn increases their liquidity as the bonds are exchanged for balances (these trades are termed open market operations). When banks have more liquid funds to loan out, this reduces the rate they charge each other for funds (in other words, the FF rate falls). Alternatively, if the Fed wishes to raise the FF rate, it will sell government bonds, reducing banks’ liquidity as they trade the bonds for balances. Open market operations are decided by the Federal Open Market Committee (FOMC) which meets eight times a year to determine a target for the FF rate. Although the FF rate is an interbank rate, it has the potential to influence the interest rates faced by consumers such as the prime rate, mortgages, loans, and savings rate. Intuitively, a bank’s lending rate will be related to the rate at which itself can borrow.

When should rates rise? When should they fall? Among other responsibilities, the Fed has a dual mandate set forth by Congress. The dual mandate is price stability and economic growth. If economic growth is in jeopardy, such as during a pandemic, the Fed will cut interest rate and provide necessary liquidity. If price stability is a concern, as is the case in 2022, the Fed will raise interest rates to reduce demand and tame inflation.

The Fight Against Inflation

For policymakers to fight inflation, some short-term economic pain and slowdown are inevitable in order to achieve long term economic stability. To minimize economic pain, the fiscal policy (set by Congress and the current Administration) must work in the same direction as monetary policy (set by the Fed). To that end, the Inflation Reduction Act was passed in 2022. The $437 billion spending package is expected to raise $737 billion in revenue and reduce net federal expenditures by $300 billion over the next decade, in hopes of reigning in the government budget deficit. Cutting the deficit can at times have the effect of dampening inflation if it reduces overall demand of goods and services and take pressure off the prices. Most of the additional revenue will be raised through a 15% corporate minimum tax rate and through prescription drug price reform allowing Medicare to negotiate the price of certain prescription drugs starting in 2026. Such a reform is welcome news given the high levels of the U.S. health care spending. However, the act packs the biggest punch in its environmental goals. $369 billion of subsidies and tax credits are to be allocated over the decade on electric vehicles (EV), renewable energy, carbon capture, and other climate change combating measures. For example, the IRA includes a subsidy of $7,500 for purchasing of EV for the lower end models and a requirement that 40% of battery components for EV be sourced from factories in the U.S. or its free trade agreement partners and that batteries be U.S. made by 2029. This is primarily to phase out Chinese components and minerals.

The IRA should have a favorable effect on cutting the U.S. greenhouse-gas emissions, but its effect on inflation will not be immediate. The Fed has the primary responsibility to reduce inflation. The Fed raised benchmark federal-funds rate six times this year (to a range between 3% and 4% from near zero, as can be seen in panel (b) of Figure 2). By raising borrowing costs and making it more costly to finance homes, cars, and business investment with higher interest rates, the Fed can curb demand for goods and services and relieve pressure off prices to further increase. In fact, the higher mortgage rates have slowed down the housing market. Housing starts and residential permits both fell on a national level.

The Fed is also hoping that a cooling down in the labor market can remove pressure off prices. And although showing some signs of loosening, labor markets remain tighter than they have ever been, with record rates of quits and job openings. Labor market tightness is sometimes measured by the number of vacant jobs compared to the number of workers available. A tight labor market favors workers. One reason for this tightness is that during the pandemic, labor market participation decreased due to many reasons such as early retirement, lack of childcare options, health concerns, and change in preferences. Another reason could be the change in the nature of available jobs during the pandemic. Labor market participation has not rebounded; therefore, the supply side of the labor market remains low. The demand for labor (vacancies) may decline as the Fed hikes interest rates. Indeed, initial jobless claims showed a slight increase signaling perhaps an increase in layoffs (but are still low enough to signaling a still strong labor market). Vacancies and new jobs have slowed down in September.

“Inflation is always and everywhere a monetary phenomenon” -Milton Friedman

As the Fed raises interest rates, reducing aggregate demand for goods and services, we expect a slowdown in economic growth and an increase in the unemployment rate. This is the price of stability: reducing aggregate demand with higher borrowing costs slows down economic activity and reduces employment but takes pressure off prices to further rise. Nonetheless, some economists would argue that even if the Fed does not raise rates, a slowdown might ensue as the expansionary effects of monetary (and fiscal) policy undertaken in the previous two years dissipate.

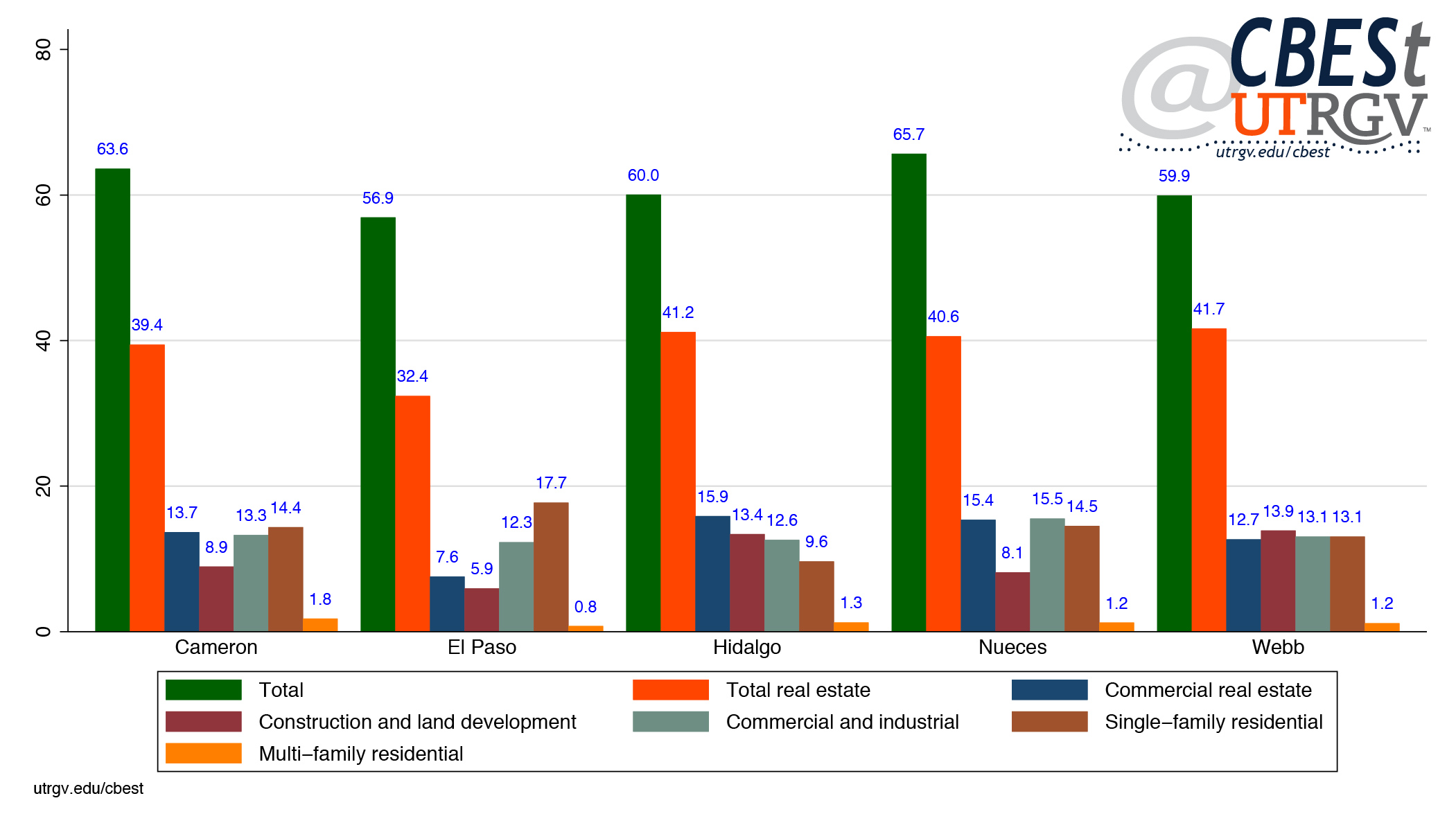

Regional Outlook

The changes taking place on a national level have had an effect on some sectors in Hidalgo County. Given its interest sensitive nature, the housing sector has experienced some shifts. Since the Federal reserve’s interest rate hike in March 2022, months in inventory has steadily increased reaching 3.9 in October of 2022, as can be seen in the Table 1. This is above the level seen last October when months in inventory was 2.4. Median home prices were stable (or slightly up) and single-family housing construction permits has steadily decreased since August. Permits, which are obtained before construction, are an indicator of future housing market conditions. This is to be expected as mortgage rates climb with the Fed’s raising of interest rates.

| Month/Year | Sales | Dollar Volume | Average Price | Median Price |

Total Listings | Months In Inventory |

Building Permit (Single Family) |

|---|---|---|---|---|---|---|---|

| 21-Oct | 325 | 74,992,709 | 230,747 | 200,000 | 861 | 2.4 | 512 |

| 21-Nov | 303 | 69,480,703 | 229,309 | 205,000 | 917 | 2.6 | 350 |

| 21-Dec | 362 | 84,411,566 | 233,181 | 218,750 | 828 | 2.4 | 375 |

| 22-Jan | 358 | 80,040,787 | 223,578 | 200,500 | 780 | 2.2 | 388 |

| 22-Feb | 350 | 77,934,240 | 222,669 | 205,000 | 731 | 2 | 290 |

| Post Monetary Tightening | |||||||

| 22-Mar | 409 | 100,166,775 | 244,907 | 215,000 | 716 | 1.9 | 385 |

| 22-Apr | 378 | 95,406,508 | 252,398 | 220,750 | 782 | 2.1 | 397 |

| 22-May | 408 | 102,359,297 | 250,881 | 228,150 | 845 | 2.3 | 402 |

| 22-Jun | 395 | 101,115,003 | 255,987 | 231,250 | 974 | 2.6 | 355 |

| 22-Jul | 338 | 84,694,764 | 250,576 | 230,000 | 1101 | 3 | 320 |

| 22-Aug | 383 | 95,084,719 | 248,263 | 220,000 | 1212 | 3.3 | 336 |

| 22-Sep | 324 | 79,412,623 | 245,101 | 228,500 | 1331 | 3.7 | 301 |

| 22-Oct | 323 | 77,484,495 | 239,890 | 225,000 | 1416 | 3.9 | 279 |

| Average | 358 | 86,352,630 | 240,576 | 217,531 | 961 | 3 | 361 |

The labor market in the region remains fairly strong and stable with unemployment mirroring those before the pandemic levels (see Table 2). From June 2021 to June 2022, average weekly wages grew by 5.10% in Hidalgo County and by 7.80% in Cameron County. The wage growth has barely kept up with inflation over the past year in the region, although this is not evident on a national level where wages grew at a rate of slower than inflation implying a reduction in real wages, as reported in Table 3.

| Brownsville-Harlingen | McAllen-Edinburg-Mission | Texas | |

| Early 2020 levels | |||

| 2020-Feb | 5.5 | 6.4 | 3.5 |

| 2020-Mar | 8.2 | 9.6 | 5.1 |

| Post Monetary Tightening | |||

| 2022-Mar | 6.1 | 7.0 | 4.4 |

| 2022-Apr | 5.9 | 6.8 | 4.3 |

| 2022-May | 6.0 | 6.9 | 4.2 |

| 2022-Jun | 6.9 | 8.1 | 4.1 |

| 2022-Jul | 6.8 | 8.0 | 4.0 |

| 2022-Aug | 6.4 | 7.6 | 4.1 |

| 2022-Sep | 5.8 | 6.7 | 4.0 |

| County | 12-month percent change in employment Total | 12-month percent change in average weekly wage Total |

| Hidalgo | 3.7% | 5.1% |

| Cameron | 3.9% | 7.8% |

| Texas | 5.2% | 6.1% |

| U.S. | 4.0% | 4.3% |

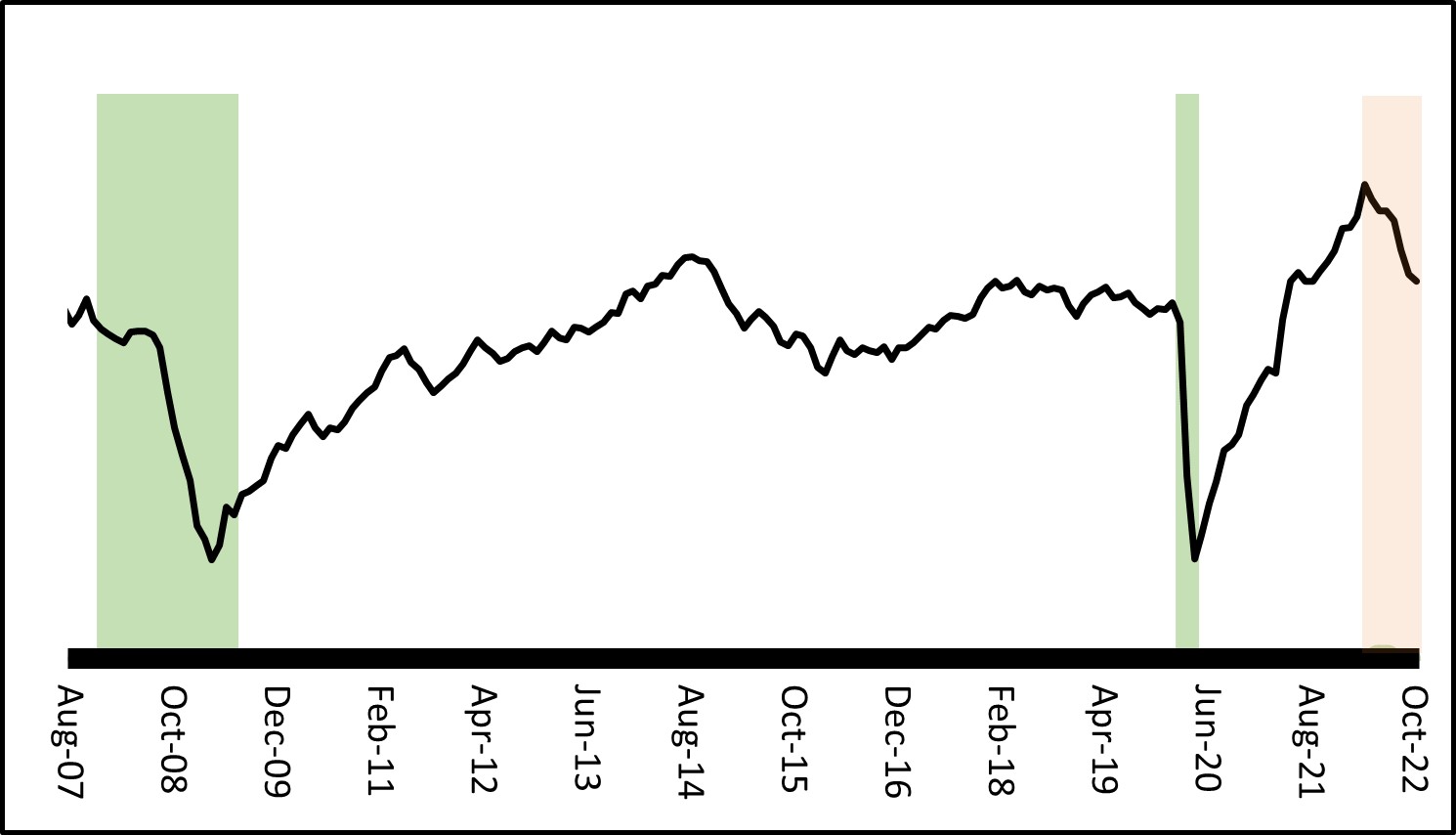

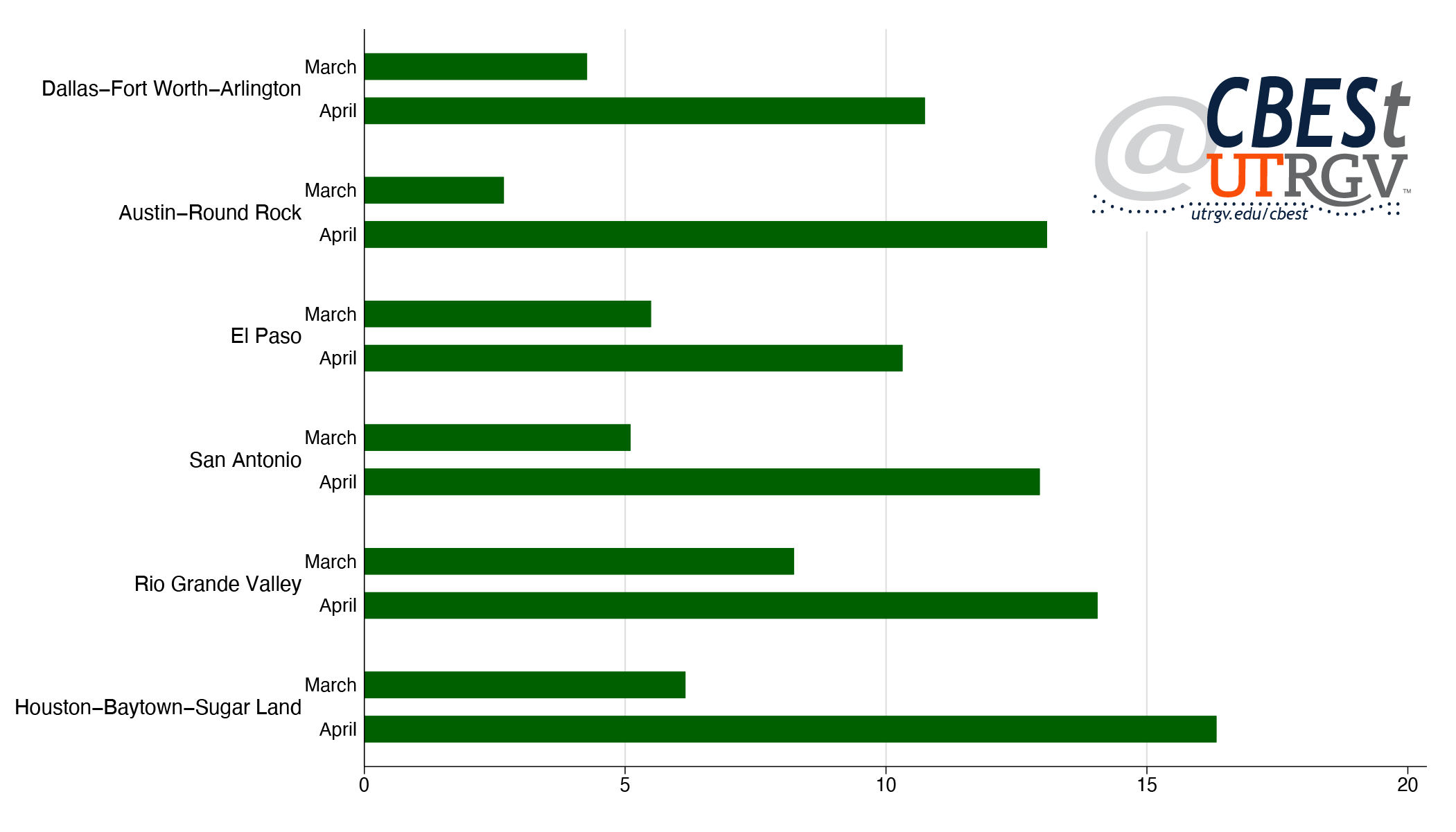

To forecast the region’s economic outlook, economists typically look at leading economic indicators. These indicators are variables that tend to decrease before overall economic activity slows down and rebound before a recovery. For Texas, the Dallas Fed combines into a single index eight indicators including the Texas value of the dollar, U.S. leading index, real oil price, well permits, initial claims for unemployment insurance, Texas stock index, help-wanted index and average weekly hours worked in manufacturing. Despite the strong labor market, the Texas Leading Index shows some signs of a slowdown since the monetary tightening by the Fed as can be seen in Figure 3. It is worth noting that the leading indicators did not pick up earlier recessions with significant lead time as can be seen in Figure 3.

Figure 3: The Dallas Fed Texas Leading Economic Indicators

Green areas indicate recessions, orange area indicates period of monetary tightening.

Source: The Dallas Fed

Summary

The Fed has shown a commitment to keeping rates high and prioritizing price stability. The effects of monetary tightening have been felt as the 12-month inflation rate was 7.1% in November, down from 9.1% in June. On December 14th, 2022, the Fed announced a 0.50 percentage point hike for the FF rate to be between 4.25% to 4.50% (compared to 1.5% to 1.75% in June). This is lower than some hikes earlier this year of .75 percentage point each.

Economists generally agree that the Fed should hold the course until price stability is achieved. In fact, studies covering historical disinflation episodes in several countries show that the output loss from reducing inflation was smaller, the faster the disinflation took place [2, 4]. This is referred to as the ‘cold turkey’ approach to disinflation.

____

Maroula Khraiche is an Associate Professor of Economics at The University of Texas Rio Grande Valley.

Andre Mollick is a Professor of Economics at The University of Texas Rio Grande Valley.

Endnotes

- Families First Coronavirus Response Act Will Cost $192 Billion. Committee for a Responsible Federal Budget. Apr 6, 2020.

- L. Ball. What determines the sacrifice ratio? In Monetary Policy, pages 155−−193. The University of Chicago Press, 1994.

- J. Jamerson, A. Duehren, and N. Andrews. Senate Approves Roughly $2 Trillion in Coronavirus Relief. Wall Street Journal. March 26, 2020.

- H. Katayama, N. Ponomareva, and M. Sharma. What determines the sacrifice ratio? a bayesian model averaging approach. Oxford Bulletin of Economics and Statistics, 81(5).

- N. McCarthy. What’s In The $1.9 Trillion Stimulus Package? Statista, March, 11 2021.

- E. Milstein and D. Wessel. What did the fed do in response to the covid-19 crisis. Brookings Institution, 2021.

Spring 2022 v18, n1

The end of globalization: Texas-Mexico border ports trends

Salvador Contreras

Over the past couple of years there have been hundreds if not thousands of reports suggesting that the end of globalization is upon us (for example [1]). They suggest that the benefits to trade have run their course and that one should expect a retrenchment, or at least a pause, to further expansion. Certainly, current geo-political events make the case to rethink existing alliances.

- download PDF here

The Texas Border Region, by its very nature is highly connected to international commerce. The recent, if temporary, decision by the Texas Governor to institute enhance inspections of Mexican trucks along the Texas – Mexico border reminds us that international trade is much bigger then the ports that oversee its flows or the trucks that sit hours on end patiently awaiting their turn to reach a customs officer [2]. It also affects available inventory at our local stores and the prices we pay at the counter.

In this piece we study trends in international trade between the US and its top 3 trading partners. We show a clear deceleration in said activity. We then turn our attention to the Texas-Mexico border. We show that national trade patterns are reflected in trade flows through the El Paso District and Laredo District. Finally, we take a close look at trends at each of the ports in the Laredo District. We close by analyzing the composition of goods that flow through these ports.

Top trading partners

We begin by showing trade patters between the US and its top 3 trading partners. All values are inflation adjusted using the Producer Price Index and reflect 2019 dollars. We focus on the dollar value of total trade. Total trade is defined as exports plus imports.

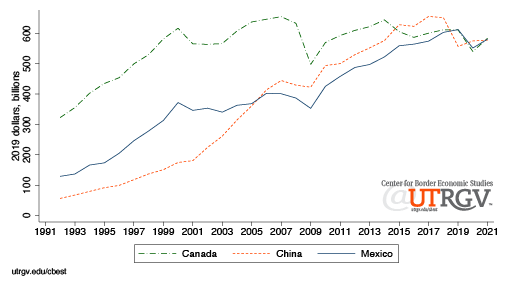

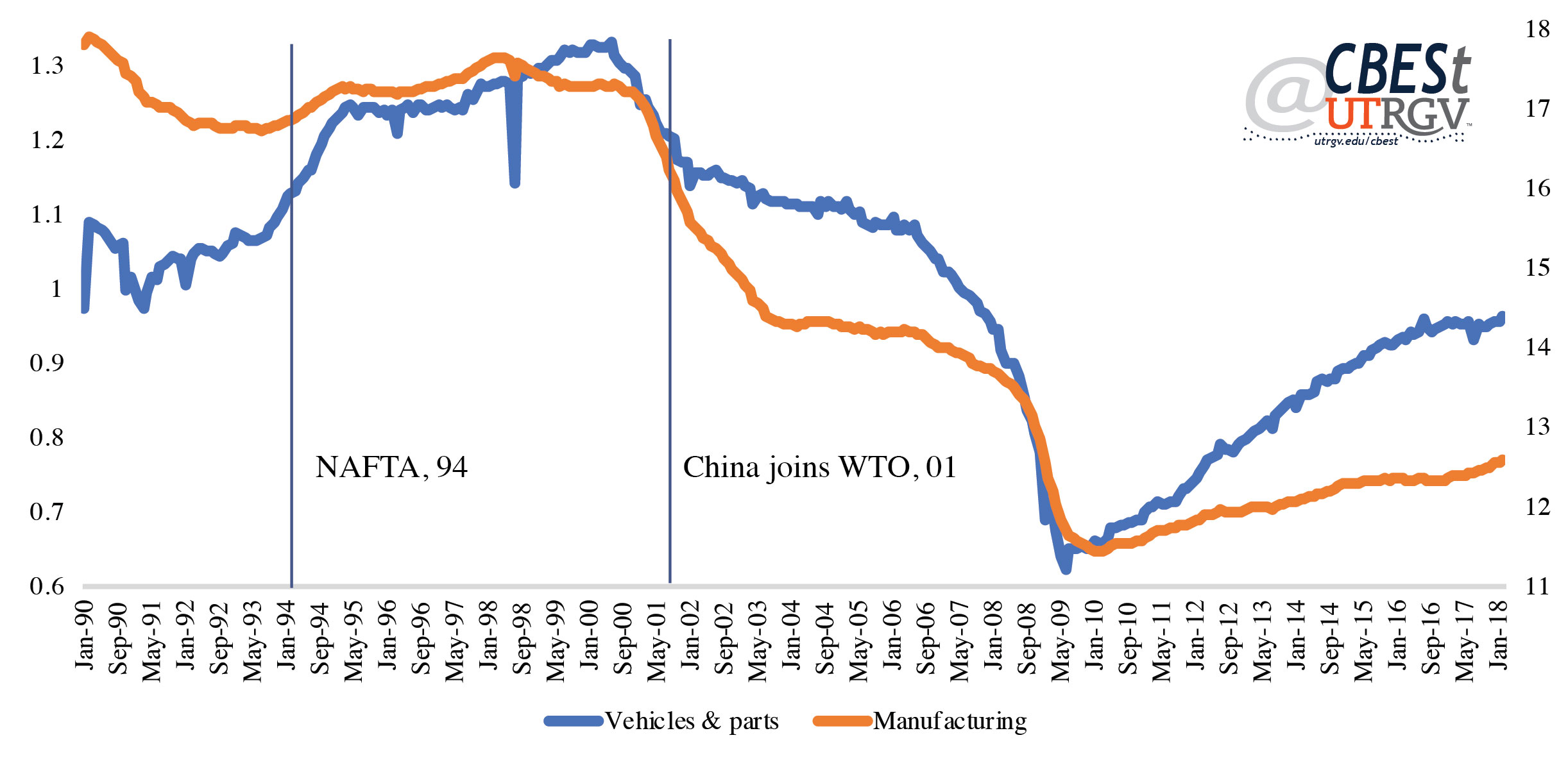

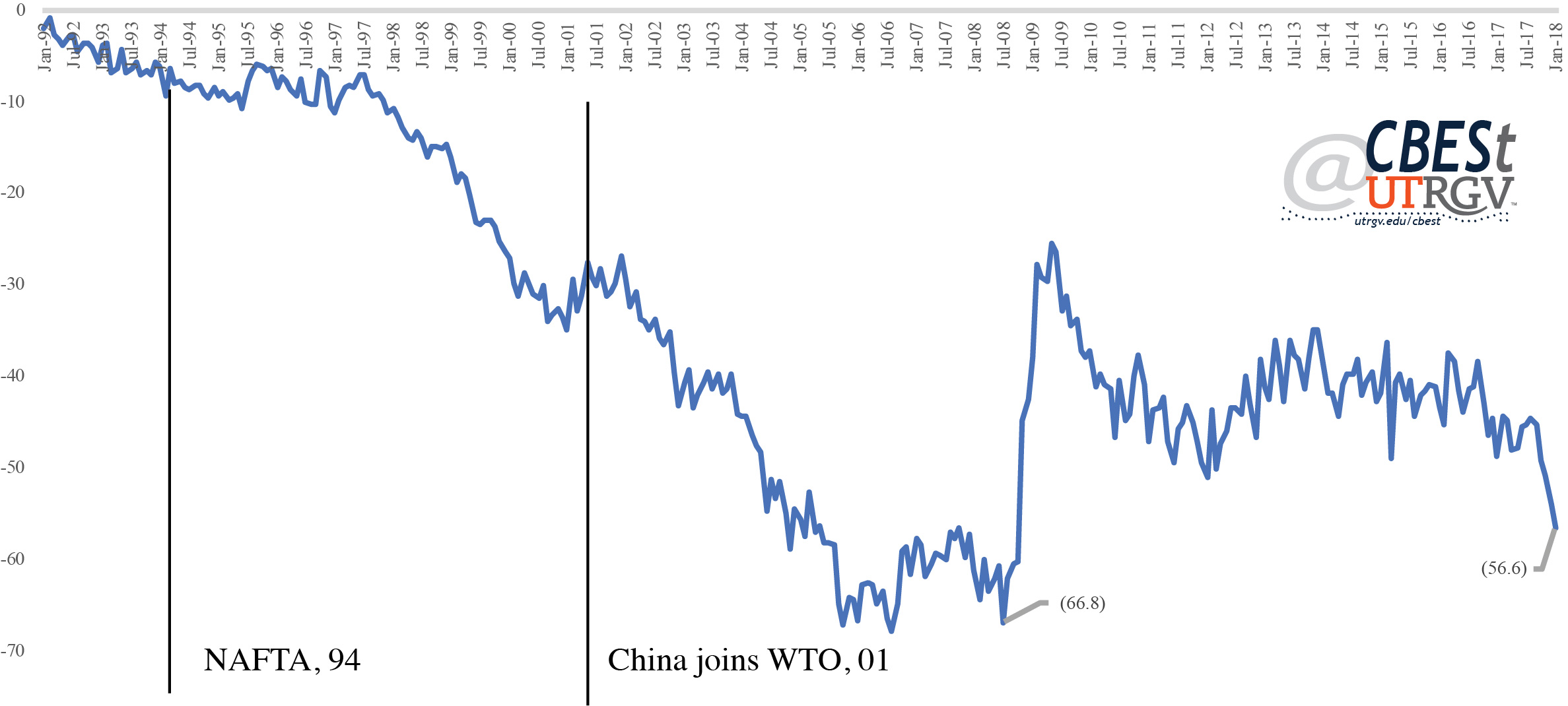

Figure 1 shows US total trade [exports + imports] with Canada, China, and Mexico. Values are in billions of dollars. Notice that from the early 1990s up to 2000 trade flows are steadily growing. In 2000 trade between Mexico and Canada begin to move sideways while trade with China continues to increase. This period coincides with China joining the World Trade Organization (WTO) in 2001. Canada total trade with the US continued to go sideways through 2021. After the 2008 Financial Crisis we see that Mexico’s trade flows keep pace with China till 2017. Days into the Trump administration’s presidency, the US pulled out of the Trans-Pacific Partnership in early 2017. This and ensuing policies to decouple the US from what were seen by some as bad trade deals can be seen in the data as a decline in trade flows with China [3]. Trade with Mexico continued to grow until the 2020 COVID lockdowns. This allowed Mexico to become the US largest trading partner in 2019. In 2021 total trade with these three countries stood around $580 billion or $1.7 trillion combined or roughly 10% of US Gross Domestic Product (GDP).

|

| Figure 1: Total trade, top 3 US trading partners Source: US Census USA Trade |

In general, trade has been trending down for the past 4 years. Is this a sign that the end of globalization is real? While, not likely. These trends suggest that it may no longer be expanding. Some argue that COVID and associated disruptions to manufacturing and supply chains is a likely culprit. Recent lookdowns of Shanghai affecting 26 million people, is a reminder that COVID is still around and that it continues to inflict damages to the world supply chain. No doubt, this is reflected in figure 1. Another reason can be placed on protectionist policies. For example, Trump era tariffs that covered a wide array of goods from steel to washing machines have also played role. In 2019, the US earned $79 billion in tariff revenue, double that of 2017 [4].

More complex explanations are geo-political in nature that thread on national security to nationalism. The Russians are reminded in their current foray of conquest that wars require basic understanding of economics and supply chain management. All the money in the world cannot buy you a microprocessor if the seller is unwilling or unable to supply it. From this view, national security arguments seem reasonable. A Brookings report states that there were some benefits to Trump era protectionist policies. For example, employment at steel and aluminum factories appears to have benefited from the use of national security (section 232) reviews. Other antidotal evidence are announcements by companies like Intel who have committed to a $20 billion investment on a new plant in Ohio or Samsung with a $17 billion investment on a Texas facility.

Yet, another explanation to these trends is that trade benefits have run their course. From the time China joined the WTO till about a few years ago, American consumers enjoyed persistent low levels of inflation. For example, in the 1990s inflation, stripping out Food and Energy, averaged 3%, 2% in the 2000s, and 1.9% in the 2010s. In 2021 it averaged 3.6%, 2022 already promises to be above 2021. Low-cost foreign labor and global commodities have benefited Americans over the past 3 decades. However, there are signs that this may be coming to an end. Chinese Industrial Production Prices grew on average by 1.3% over 2000 to 2020. From January 2021 to March 2022 price growth has averaged 8.2%. The US is pushing companies to bring jobs back at a time when costs of producing in China and elsewhere are rising. American’s own recent inflation trends in part reflect this story.

US trade with its top trading partners has stopped growing. It happens to coincide with a period of disappearing cost advantages to offshoring. Globalization continues to have a pulse. What is different now is that margins from trade to both consumers and businesspersons have begun to shrink. These trends will likely make it easier for protectionist voices to get a seat at the policymaking table. Next, we turn to the Texas-Mexico border region.

Texas Border

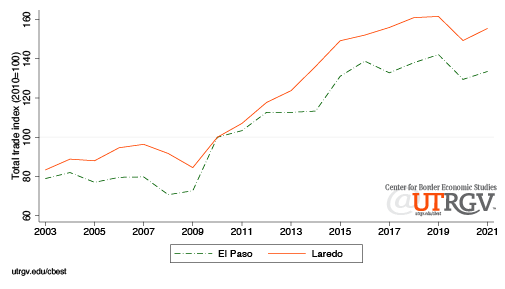

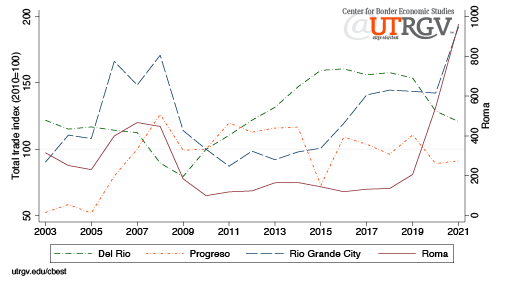

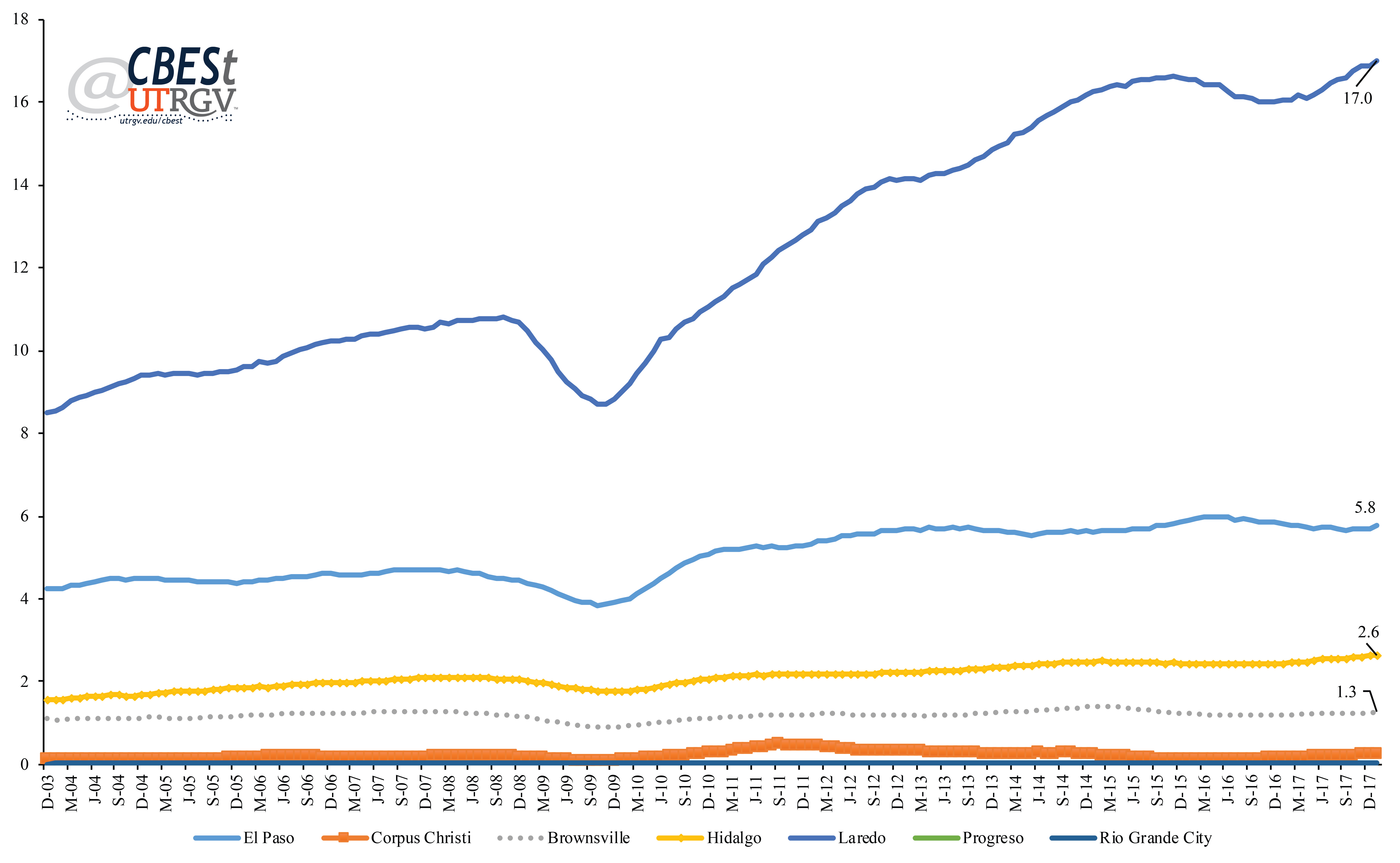

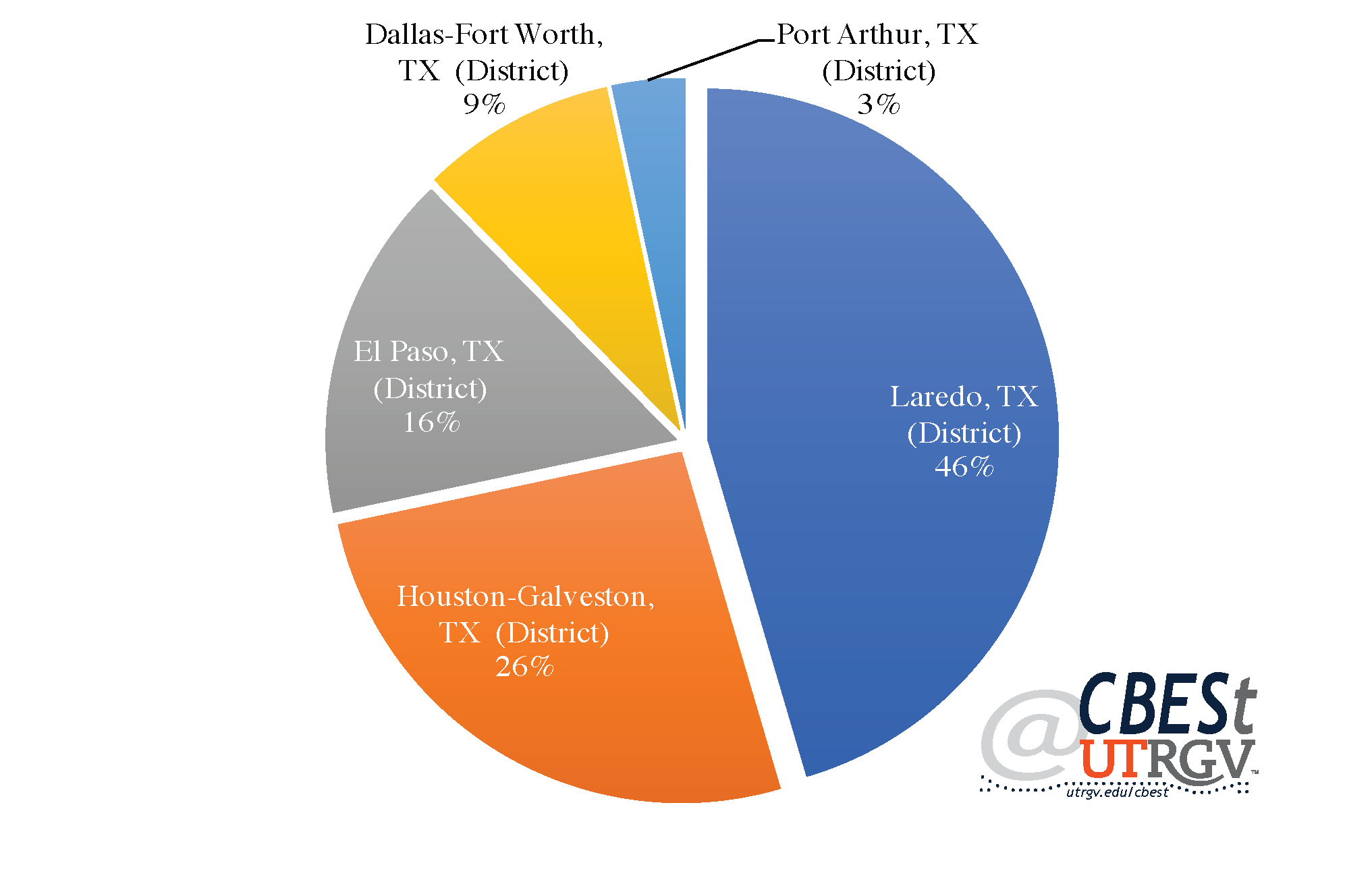

The El Paso District and the Laredo District cover all Texas land ports with Mexico. In 2021, the Laredo District handled $310 billion in total trade. For comparison, the El Paso District handled $103 billion. Figure 2 shows the two districts total trade index. We set 2010 as the reference year. The figure tells us that total trade prior to the Financial Crisis period was not growing. After 2009, trade flows accelerated for about 6 years. Then, we see a deceleration that continues today. This is consistent with the general trends we observed in figure 1.

|

| Figure 2: Total trade through Texas border port districts Source: US Census USA Trade |

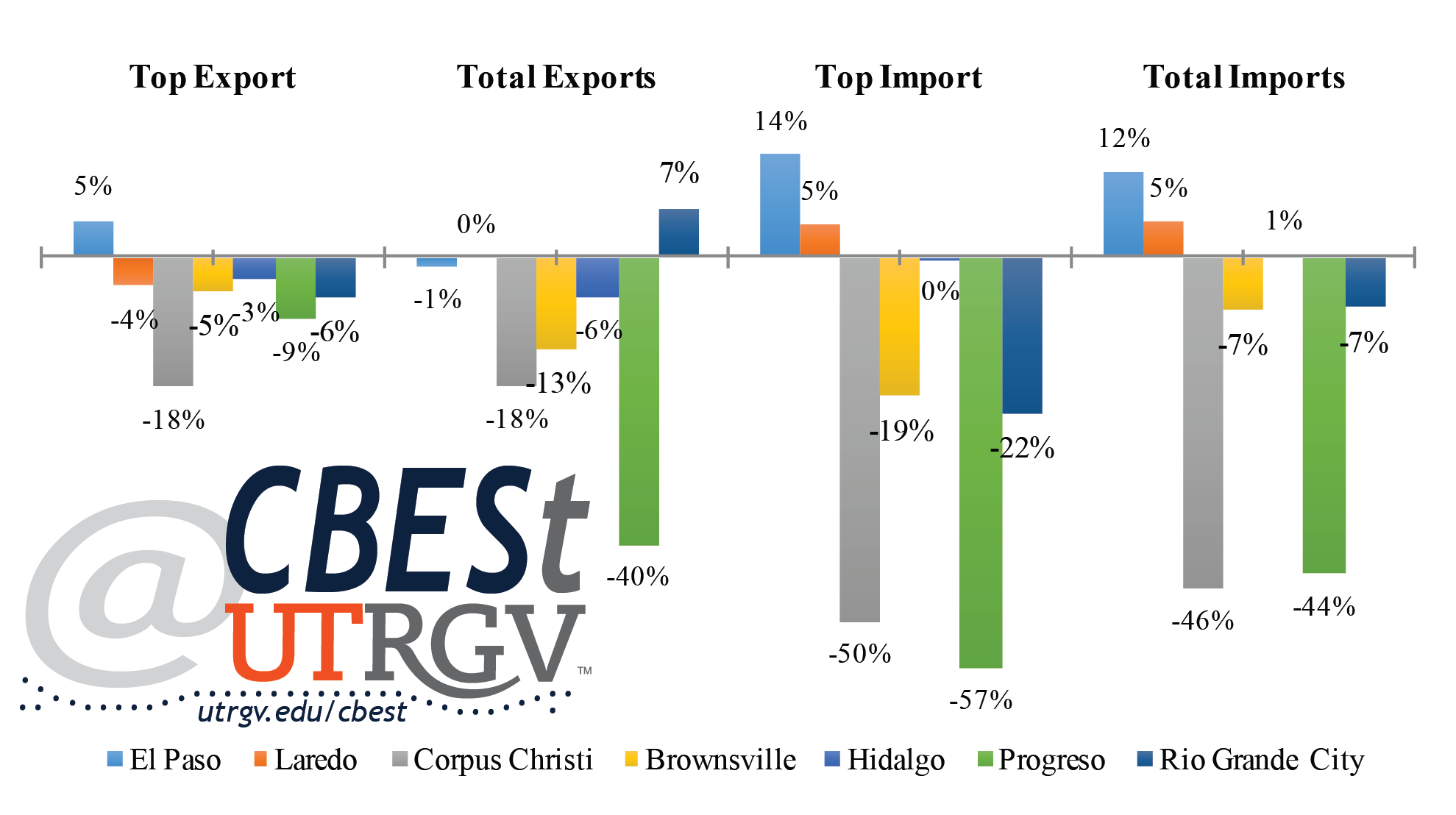

In 2021 total trade in the El Paso District and the Laredo District was 34% and 56% above 2010 levels, respectively. Trade peaked in 2019, the El Paso District and Laredo District enjoyed $110 billion and $322 billion in total trade, respectively.

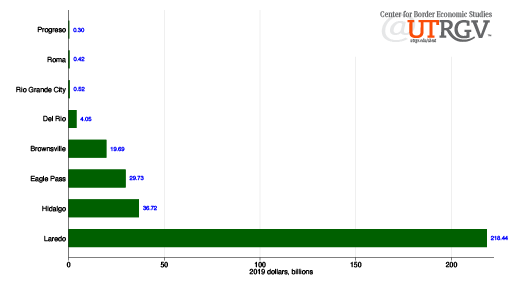

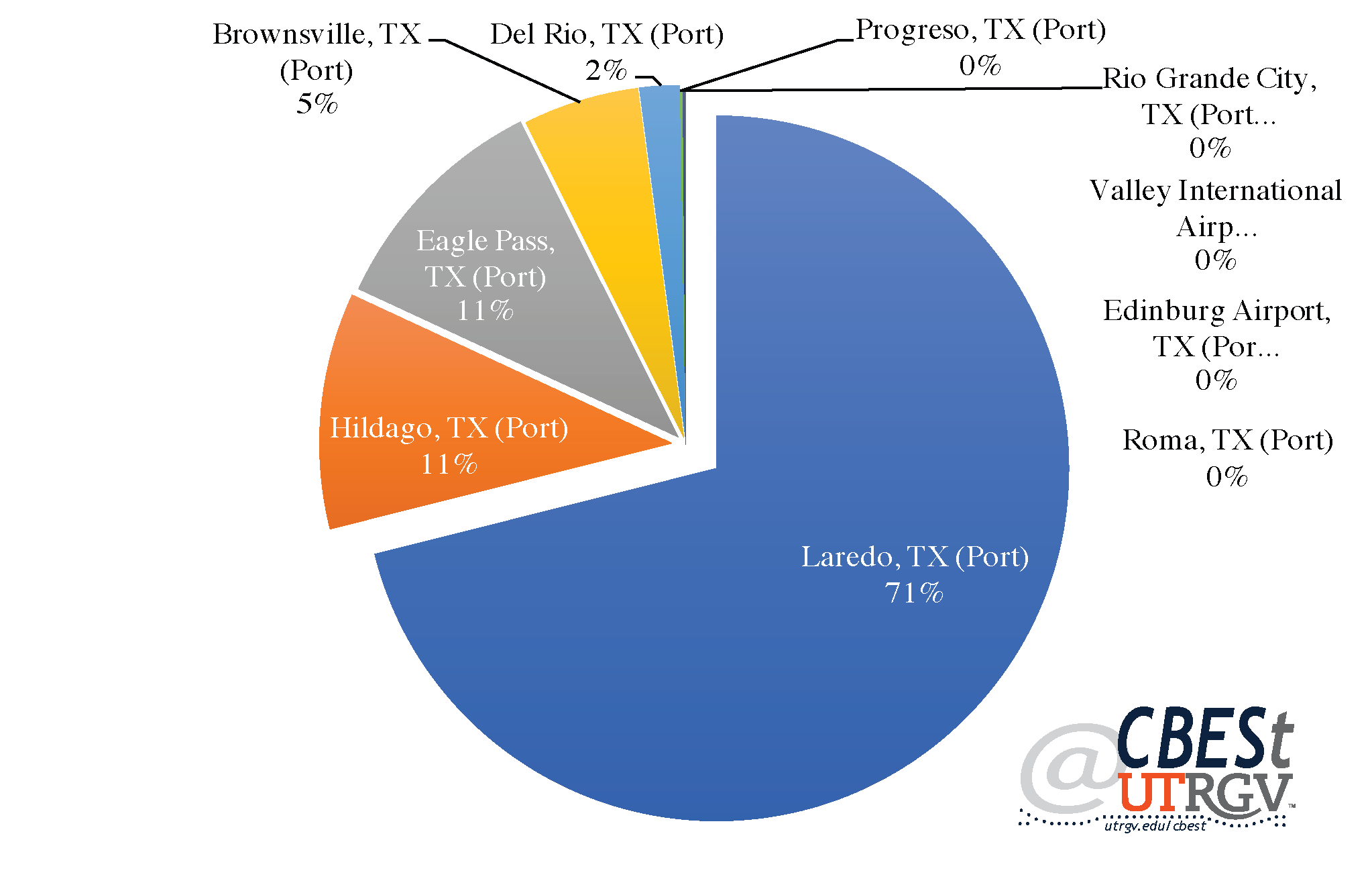

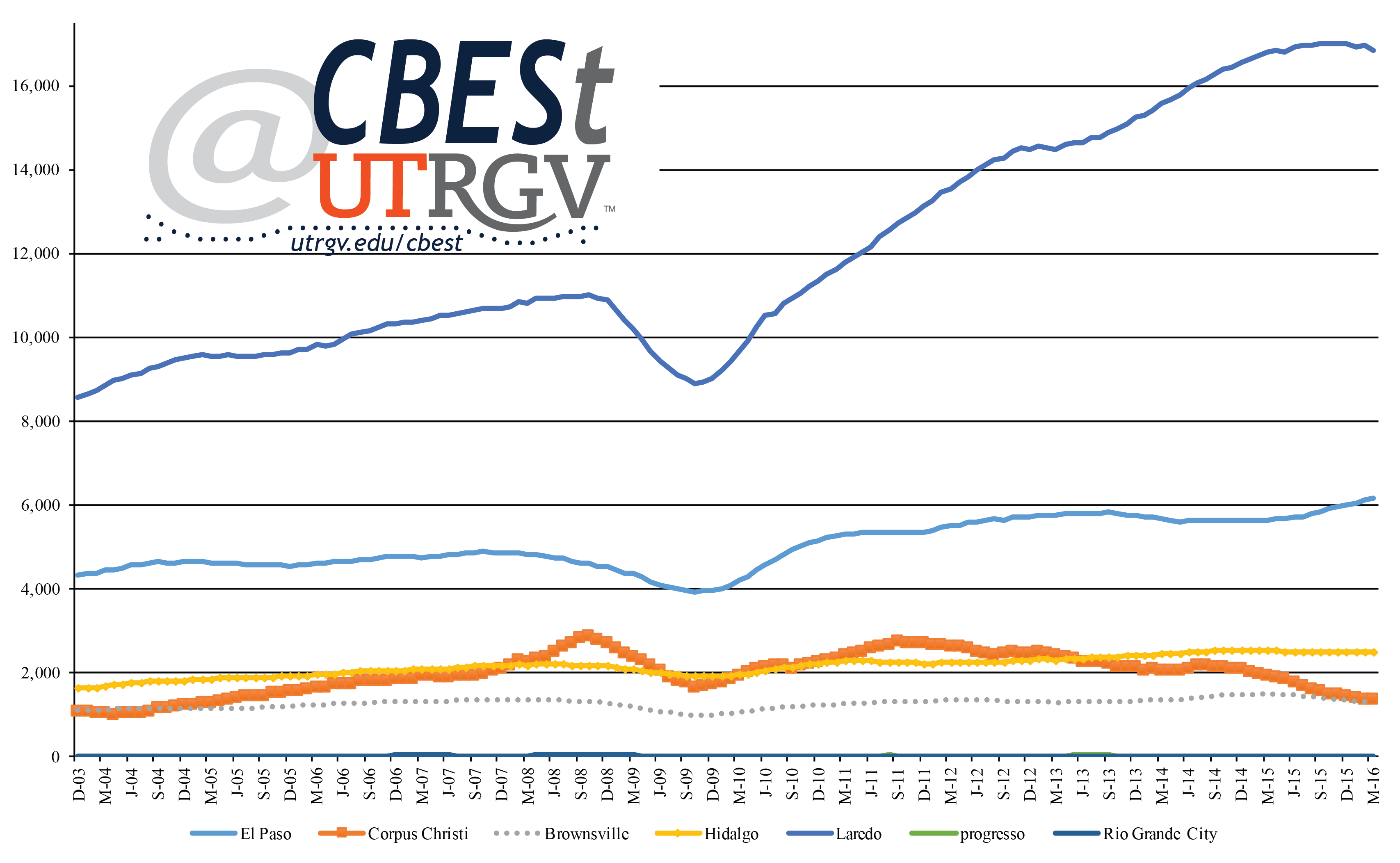

The Laredo District is made up of the Port of Brownsville, Port of Del Rio, Port of Eagle Pass, Edinburg Airport, Port of Hidalgo, Port of Laredo, Port of Progreso, Port of Rio Grande City, Port of Roma, and Valley International Airport (Harlingen). We will not report on Edinburg Airport and briefly on Valley International Airport. These two ports are small and do not have trade figures in all the years of analysis. Figure 3 shows the inflation adjusted value of total trade through Laredo District ports.

The Port of Laredo is the district’s largest port. It accounts for 70% of district total. At distant second is the Port of Hidalgo that accounts for $37 billion or 12% of district total. The Port of Eagle Pass and Brownsville round up the largest 4 ports. The Port of Progresso is the district’s smallest port. In 2021 it handled $304 million. Followed by the Port of Roma at $415 million.

|

| Figure 3: 2021 total trade by port Source: US Census USA Trade |

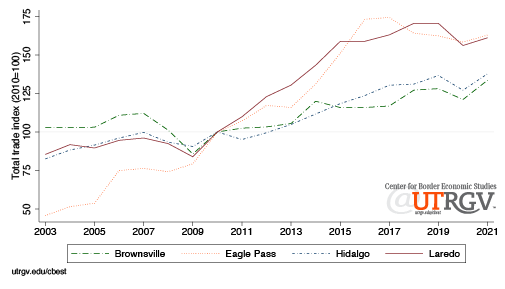

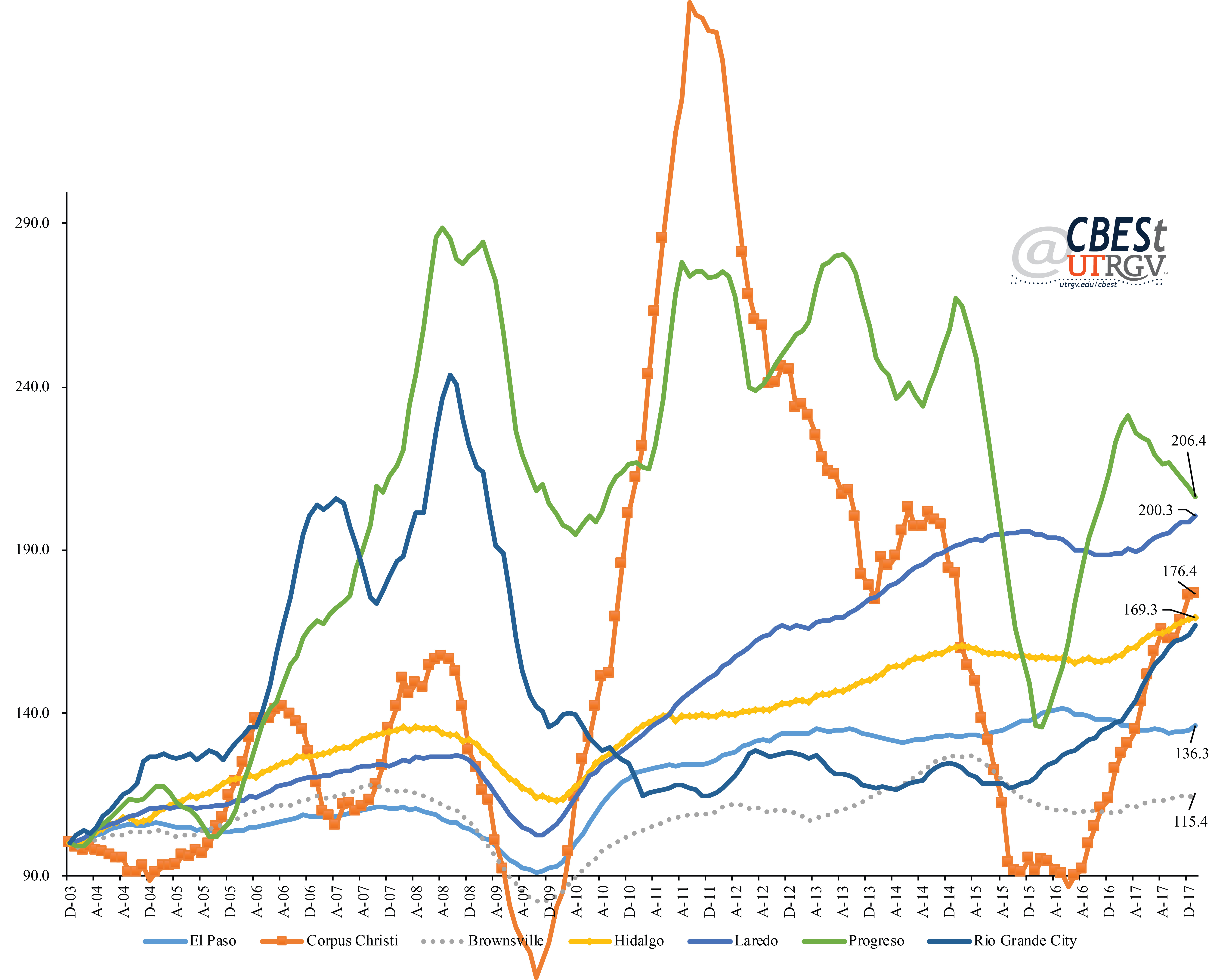

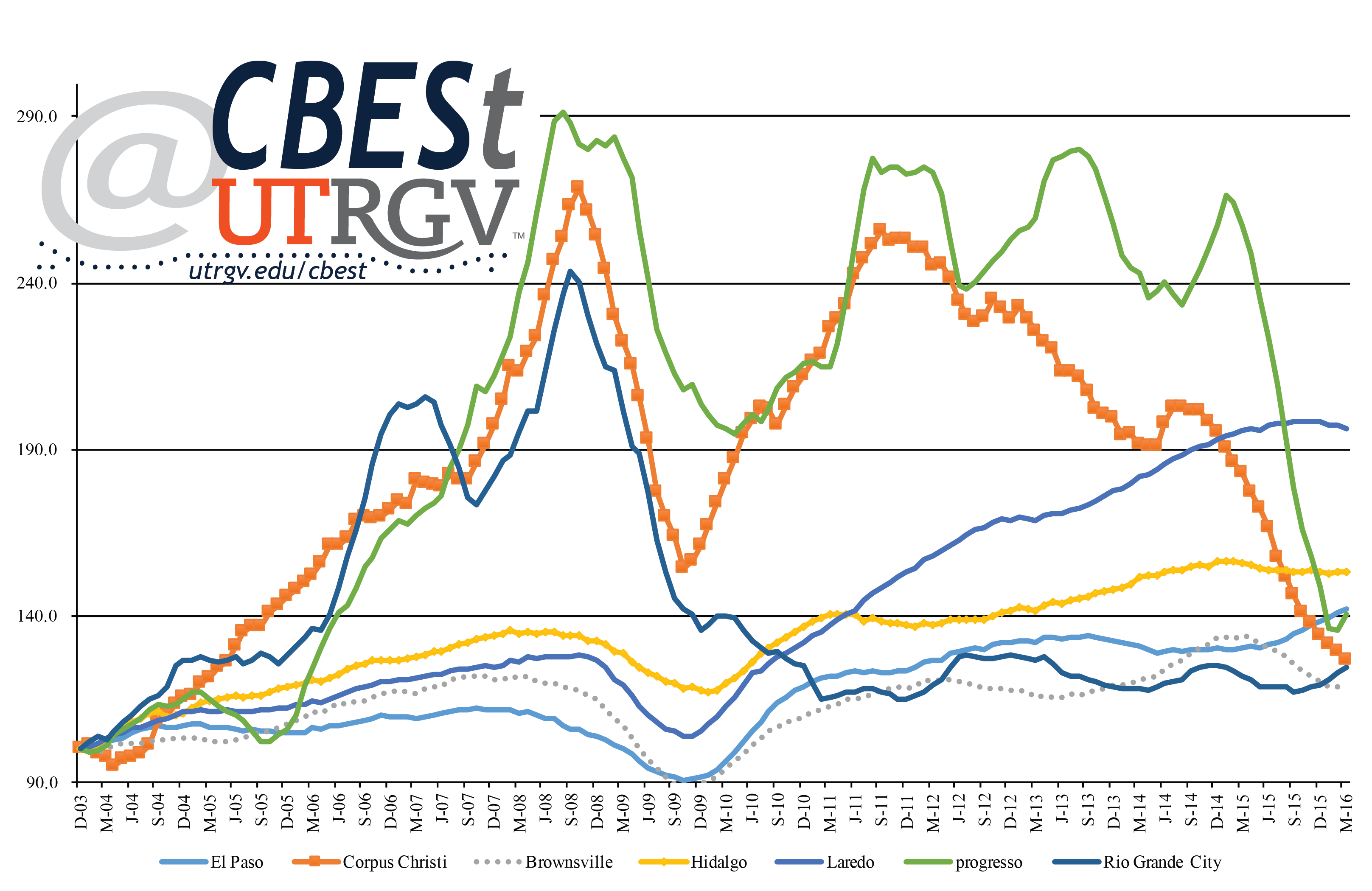

Figure 4 presents total trade index for the largest ports in the Laredo District. The index is normalized to 100 in 2010 and is based on inflation adjusted port level total trade. The Port of Eagle Pass and Port of Laredo saw the highest growth over the past 10 years. However, notice that these ports reflect zero growth over the past 5 years, like national trends. In 2021, the Port of Eagle Pass and Port of Laredo were 63% and 61% above 2010 levels, respectively. The Port of Brownsville and Port of Hidalgo have seen a steady upward movement in trade flows over the past 10 yeas. In 2021 these ports were 34% and 38% above their 2010 levels, respectively.

|

| Figure 4: Laredo District, large ports Source: US Census USA Trade |

Figure 5 presents the total trade index for the small ports in the Laredo District. The Port of Roma has the largest increase. For this reason, the values for the Port of Roma appear on the right-axis (all others, left-axis). In 2021, the Port of Roma moved 10 times the value it handled in 2010. This impressive growth occurred in the past 3 years. The Port of Rio Grande City observed the second largest end of period growth. In 2021 total trade was under 2 times larger than 2010. The only port to see no growth over the past decade is the Port of Progreso. It ended 2021 9% below its 2010 level.

|

| Figure 5: Laredo District, small ports Source: US Census USA Trade |

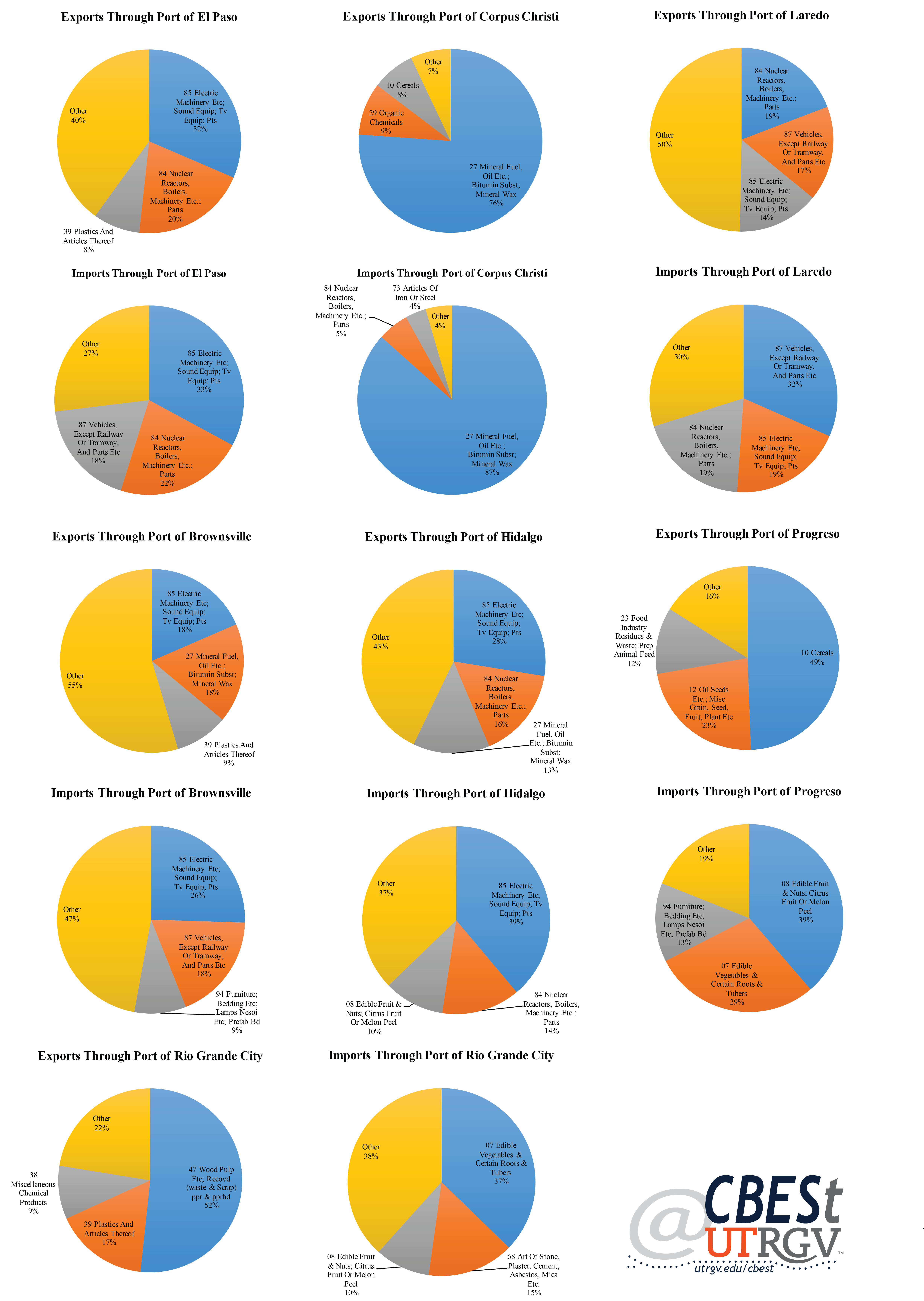

Composition of goods

Next, we present the categories of goods that cross the El Paso District and Laredo District. Categories are based on the Harmonized System (HS) codes. We present both 2-digit and 6-digit categories. The 2-digits correspond to the chapter or broad category. The item can be further detailed by their heading with two additional digits and subheading with an additional two digits. Table 1 presents the 2021 share of total trade by chapter category (2-digit). For example, HS 84 “Nuclear reactors, boilers, machinery, and mechanical appliances; parts thereof” represents 36% of the $103 billions of total trade in the El Paso District. Of these, 11 billion was southbound and $26 billion was northbound flows, for a total of $37 billion. There is a total of 99 2-digit codes.

Table 1 presents the top 10 2-digit codes for the El Paso District and Laredo District. Notice that 75% of everything that moves through the El Paso District are in the top 4 categories. Six of the district’s 10 categories have exports exceed imports. Of the 10 categories, on net, $19 billion flow northbound. In comparison, the Laredo District appears more diversified. The top 10 categories account for 75% of total flows. In addition, both El Paso District and Laredo Districts share the same top three HS 2-digit categories 84, 85, and 87. These three account for 69% of El Paso District and 53% of Laredo District total trade. The Laredo District’s top two categories account for $115 billion in total trade.

| Table 1: 2021 El Paso District and Laredo District share of total trade, top 10 categories (2-digit) Source: US Census USA Trade |

| Million (2019 dollars) | |||||

| District | Harmonized System Code | Exports | Imports | Total trade | Share of total trade (%) |

| El Paso | 84 Nuclear reactors, boilers, machinery and mechanical appliances; parts thereof | 10,894.7 | 26,208.0 | 37,102.6 | 36.0 |

| El Paso | 85 Electrical machinery and equipment and parts thereof; sound recorders and reproducers, television image and sound recorders and reproducers, and parts and accessories of such articles | 13,342.5 | 12,400.8 | 25,743.2 | 25.0 |

| El Paso | 87 Vehicles other than railway or tramway rolling-stock, and parts and accessories thereof | 1,094.0 | 6,828.2 | 7,922.2 | 7.7 |

| El Paso | 90 Optical, photographic, cinematographic, measuring, checking, precision, medical or surgical instruments and apparatus; parts and accessories thereof | 1,612.1 | 5,178.4 | 6,790.5 | 6.6 |

| El Paso | 39 Plastics and articles thereof | 2,330.3 | 819.5 | 3,149.9 | 3.1 |

| El Paso | 27 Mineral fuels, mineral oils and products of their distillation; bituminous substances; mineral waxes | 3,026.3 | 0.5 | 3,026.8 | 2.9 |

| El Paso | 94 Furniture; bedding, mattresses, mattress supports, cushions and similar stuffed furnishings; lamps and lighting fittings, not elsewhere specified or included; illuminated signs, illuminated name-plates and the like; prefabricated buildings | 173.9 | 1,964.4 | 2,138.3 | 2.1 |

| El Paso | 73 Articles of iron or steel | 746.6 | 432.4 | 1,179.0 | 1.1 |

| El Paso | 10 Cereals | 1,001.2 | 3.8 | 1,005.0 | 1.0 |

| El Paso | 74 Copper and articles thereof | 744.4 | 112.9 | 857.3 | 0.8 |

| Laredo | 87 Vehicles other than railway or tramway rolling-stock, and parts and accessories thereof | 12,449.4 | 51,908.3 | 64,357.7 | 20.8 |

| Laredo | 84 Nuclear reactors, boilers, machinery and mechanical appliances; parts thereof | 17,991.9 | 32,861.6 | 50,853.5 | 16.4 |

| Laredo | 85 Electrical machinery and equipment and parts thereof; sound recorders and reproducers, television image and sound recorders and reproducers, and parts and accessories of such articles | 14,886.4 | 33,863.7 | 48,750.1 | 15.7 |

| Laredo | 27 Mineral fuels, mineral oils and products of their distillation; bituminous substances; mineral waxes | 16,451.6 | 381.6 | 16,833.2 | 5.4 |

| Laredo | 39 Plastics and articles thereof | 11,248.5 | 4,177.4 | 15,425.9 | 5.0 |

| Laredo | 73 Articles of iron or steel | 3,552.5 | 4,416.2 | 7,968.6 | 2.6 |

| Laredo | 94 Furniture; bedding, mattresses, mattress supports, cushions and similar stuffed furnishings; lamps and lighting fittings, not elsewhere specified or included; illuminated signs, illuminated name-plates and the like; prefabricated buildings | 911.4 | 6,599.3 | 7,510.7 | 2.4 |

| Laredo | 90 Optical, photographic, cinematographic, measuring, checking, precision, medical or surgical instruments and apparatus; parts and accessories thereof | 2,590.1 | 4,298.8 | 6,889.0 | 2.2 |

| Laredo | 22 Beverages, spirits and vinegar | 192.8 | 6,380.0 | 6,572.8 | 2.1 |

| Laredo | 8 Edible fruit and nuts; peel of citrus fruit or melons | 79.5 | 5,487.9 | 5,567.3 | 1.8 |

Table 2 presents the more disaggregated 6-digit categories for all ports in the Laredo District (except Edinburg Airport). We present the top 5 goods. For example, the top category through the Port of Brownsville is HS 271019, “Petroleum oils and oils from bituminous minerals, not containing biodiesel, not crude, not waste oils; preparations n.e.c, containing by weight 70% or more of petroleum oils or oils from bituminous minerals; not light oils and preparations.” The Port of Brownsville saw $2.6 billion flow southbound and $286 million northbound. This good accounts for 14.5% of the port’s $19.7 billion in total trade. Three of the top 5 categories in the port are in HS 27. The oil and gas sector accounts for a quarter of the port’s total trade. More importantly, these are mainly southbound flows. Table 2 also shows that natural gas is an important commodity accounting for $1.4 billion and $4.2 billion of southbound flows through the Port of Brownsville and the Port of Hidalgo, respectively.

In February avocados were temporary barred from entering the US because of a threatening phone call made to a US inspector in the state of Michoacan [5]. More recently, Governor Abbot’s decision to order enhanced inspections of trucks crossing from Mexico caused much concern about potential losses of perishable goods such as avocados and tomatoes [6]. Table 2 shows that $1.4 billion worth of avocados crossed through the Port of Hidalgo and $20 million the Port of Progreso. In addition to $52 million in lemons through the Port of Progreso, $41 million in peppers and pimento through the Port of Rio Grande City, and $81 million in tomatoes and $40 million in vegetables through the Port of Roma. In all, about $1.7 billion in perishable produce crossed through the southern part of the Laredo District.

Table 2 shows that 4 of the 5 top 6-digit categories in the Port of Laredo are in HS 87. Indeed, 3 of the 5 categories in the Port of Eagle Pass are in HS 87. It shows that the northern part of the district mostly moves components associated with the transportation industry. In addition, among the top three district’s ports, the Port of Laredo is the most diversified, followed by the Port of Hidalgo, and the Port of Eagle Pass is the least. The top 5 6-digit commodities account for 53% of the Port of Eagle Pass total trade, 27% of the Port of Hidalgo and 14% of the Port of Laredo.

| Table 2: 2021 Port level share of total trade, top 5 categories (6-digit) Source: US Census USA Trade |

| Millions of 2019 dollars | |||||

| Port | Harmonized System Code | Exports | Imports | Total trade | Share of total trade (%) |

| Brownsville | 271019 Petrol Oil Bitum Mineral (nt Crud) Etc Nt Biodiesl | 2,562.0 | 286.4 | 2,848.3 | 14.5 |

| Brownsville | 271121 Natural Gas, Gaseous | 1,392.7 | 0.0 | 1,392.7 | 7.1 |

| Brownsville | 852351 Solid-state Non-vol Semiconductor Storage Devices | 1.4 | 1,063.7 | 1,065.1 | 5.4 |

| Brownsville | 271012 Lt Oils, Preps Gt=70% Petroleum/bitum Nt Biodiesel | 734.1 | 0.0 | 734.1 | 3.7 |

| Brownsville | 847330 Parts & Accessories For Adp Machines & Units | 54.9 | 502.3 | 557.2 | 2.8 |

| Del Rio | 940190 Parts Of Seats (ex Medical, Barber, Dental Etc) | 13.6 | 480.8 | 494.4 | 12.2 |

| Del Rio | 841191 Turbojet And Turboproller Parts | 2.1 | 288.6 | 290.7 | 7.2 |

| Del Rio | 880000 Civilian Aircraft, Engines, And Parts | 247.5 | 0.0 | 247.5 | 6.1 |

| Del Rio | 870899 Parts And Accessories Of Motor Vehicles, Nesoi | 67.2 | 160.4 | 227.6 | 5.6 |

| Del Rio | 850940 Electromech Food Grinder Processor Mixer Extrctor | 74.9 | 116.9 | 191.8 | 4.7 |

| Eagle Pass | 870421 Trucks, Nesoi, Diesel Eng, Gvw 5 Metric Tons & Und | 3.2 | 4,904.9 | 4,908.1 | 16.5 |

| Eagle Pass | 870431 Mtr Veh Trans Gds Spk Ig In C P Eng, Gvw Nov 5 Mtn | 226.8 | 4,518.7 | 4,745.5 | 16.0 |

| Eagle Pass | 220300 Beer Made From Malt | 0.0 | 3,091.2 | 3,091.2 | 10.4 |

| Eagle Pass | 870323 Pass Veh Spk-ig Int Com Rcpr P Eng >1500 Nov 3m cc | 37.1 | 1,933.0 | 1,970.1 | 6.6 |

| Eagle Pass | 120190 Soybeans, Nesoi | 909.5 | 0.0 | 909.5 | 3.1 |

| Hidalgo | 271121 Natural Gas, Gaseous | 4,244.6 | 0.0 | 4,244.6 | 11.6 |

| Hidalgo | 852872 Reception Apparatus For Television, Color, Nesoi | 0.8 | 2,564.2 | 2,565.0 | 7.0 |

| Hidalgo | 080440 Avocados, Fresh Or Dried | 0.0 | 1,441.6 | 1,441.6 | 3.9 |

| Hidalgo | 853710 Controls Etc W Elect Appr F Elect Cont Nov 1000 V | 99.5 | 938.4 | 1,037.9 | 2.8 |

| Hidalgo | 271012 Lt Oils, Preps Gt=70% Petroleum/bitum Nt Biodiesel | 701.9 | 47.5 | 749.4 | 2.0 |

| Laredo | 870120 Road Tractors For Semi-trailers | 17.7 | 6,177.7 | 6,195.4 | 2.8 |

| Laredo | 870899 Parts And Accessories Of Motor Vehicles, Nesoi | 2,058.9 | 3,267.3 | 5,326.2 | 2.4 |

| Laredo | 851762 Mach For Recp/convr/trans/regn Of Voice/image/data | 809.4 | 4,512.5 | 5,321.9 | 2.4 |

| Laredo | 870829 Pts & Access Of Bodies Of Motor Vehicles, Nesoi | 1,480.9 | 3,656.0 | 5,137.0 | 2.4 |

| Laredo | 870323 Pass Veh Spk-ig Int Com Rcpr P Eng >1500 Nov 3m cc | 157.9 | 4,218.6 | 4,376.5 | 2.0 |

| Laredo | 870840 Gear Boxes For Motor Vehicles | 1,725.9 | 2,632.4 | 4,358.3 | 2.0 |

| Progreso | 100590 Corn (maize), Other Than Seed Corn | 88.7 | 0.0 | 88.7 | 29.2 |

| Progreso | 080550 Lemons And Limes, Fresh Or Dried | 0.0 | 52.2 | 52.2 | 17.2 |

| Progreso | 100610 Rice In The Husk (paddy Or Rough) | 26.0 | 0.0 | 26.0 | 8.6 |

| Progreso | 100790 Grain Sorghum, Nesoi | 25.3 | 0.0 | 25.3 | 8.3 |

| Progreso | 080440 Avocados, Fresh Or Dried | 0.0 | 20.1 | 20.1 | 6.6 |

| Rio Grande City | 680911 Plstr Brds Etc Nt Orna, Fcd W ppr O pprbrd Only | 0.0 | 58.8 | 58.8 | 11.2 |

| Rio Grande City | 730661 Tubes, Pipes Etc Irn/stl Wldd, Sq/rct Cr-sec Nesoi | 0.6 | 42.8 | 43.4 | 8.3 |

| Rio Grande City | 847989 Mach & Mechanical Appl W Individual Function Nesoi | 0.0 | 42.4 | 42.4 | 8.1 |

| Rio Grande City | 070960 Fruits Of Genus Capsicum Or Pimenta, Fresh/chilled | 0.0 | 41.2 | 41.2 | 7.9 |

| Rio Grande City | 721070 Fr Ir/nas 600mm W Om, Painted, Varnished, Plastic | 0.0 | 41.0 | 41.0 | 7.8 |

| Roma | 070200 Tomatoes, Fresh Or Chilled | 0.0 | 80.5 | 80.5 | 19.4 |

| Roma | 070999 Vegetables, Fresh Or Chilled, Nesoi | 0.0 | 40.3 | 40.3 | 9.7 |

| Roma | 220210 Waters, Incl Mineral & Aerated, Sweetnd Or Flavord | 0.0 | 28.4 | 28.4 | 6.8 |

| Roma | 851712 Phones For Cellular Ntwks Or For Oth Wireless Ntwk | 27.1 | 0.0 | 27.1 | 6.5 |

| Roma | 070490 Edible Brassicas (cabbages Etc) Nesoi, Fr Or Chill | 0.0 | 20.3 | 20.3 | 4.9 |

| VIA, Harlingen | 880000 Civilian Aircraft, Engines, And Parts | 5.4 | 0.0 | 5.4 | 68.1 |

| VIA, Harlingen | 854231 Processors And Controllers, Electronic Integ Circt | 0.0 | 0.8 | 0.8 | 10.4 |

| VIA, Harlingen | 901590 Parts And Accessories For Surveying Etc Nesoi | 0.8 | 0.0 | 0.8 | 10.4 |

| VIA, Harlingen | 850450 Electrical Inductors Nesoi | 0.0 | 0.3 | 0.3 | 3.9 |

| VIA, Harlingen | 854239 Electronic Integrated Circuits, Nesoi | 0.0 | 0.1 | 0.1 | 1.8 |

Summary

The end of globalization is probably not here. However, there are clear indications that US trade over the past few years has begun to wane. It’s hard to see what the impetus will be to get trade flows growing again. National security concerns and politics across the globe are working in favor of taming globalists ideas. The Texas border region plays an important role helping keep shelves across the US stocked. This is often forgotten when policymakers fail to consider the effects that trade policy decisions have on the Texas border. In fact, we learned from the 10 days the Texas order on enhanced inspections of Mexican trucks was in effect that individuals with little say on matters of international commerce can so easily inflict damages on trade flows and border communities [7].

____

Dr. Salvador Contreras is Associate Professor of Economics at the University of Texas Rio Grande Valley

Endnotes

[1] Justin Lahart. Globalization Isn’t Unraveling. It’s Changing. The Wall Street Journal. April 15, 2022. https://www.wsj.com/articles/globalization-isnt-unraveling-its-changing-11650015032?page=1

[2] Governor Abbott Takes Aggressive Action To Secure The Border As President Biden Ends Title 42 Expulsions. Office of the Texas Governor. April 6, 2022. https://gov.texas.gov/news/post/governor-abbott-takes-aggressive-action-to-secure-the-border-as-president-biden-ends-title-42-expulsions

[3] Jim Tankersley and Keith Bradsher. Trump Hits China With Tariffs on $200 Billion in Goods, Escalating Trade War. The New York Times. Sept. 17, 2018 https://www.nytimes.com/2018/09/17/us/politics/trump-china-tariffs-trade.html

[4] Geoffrey Gertz. Did Trump’s tariffs benefit American workers and national security? Brookings. SEPTEMBER 10, 2020. https://www.brookings.edu/policy2020/votervital/did-trumps-tariffs-benefit-american-workers-and-national-security/

[5] Anthony Harrup. Mexico Resumes Exports of Avocados to U.S. The Wall Street Journal. Feb. 18, 2022. https://www.wsj.com/articles/mexico-resumes-exports-of-avocados-to-u-s-11645213662?page=1

[6] Jason Beeferman. In McAllen, Gov. Greg Abbott’s border inspections meant late deliveries, rotten produce and lost business. The Texas Tribune. April 15, 2022. https://www.texastribune.org/2022/04/15/mcallen-greg-abbott-border-inspections/

[7] Sandra Sanchez. $1B lost due to South Texas bridge closure, truck inspections, city officials say. Border Report. Apr 18, 2022 https://www.borderreport.com/regions/texas/1b-lost-due-to-south-texas-bridge-closure-truck-inspections-city-officials-say/

Current issue: Winter 2021 v17, n4

The reach of the Paycheck Protection Program in the Lone Star State

Salvador Contreras

The Paycheck Protection Program (PPP) by some accounts was instrumental at preventing mass small business failures. The program awarded $790 billion in forgivable loans to 11 million small businesses. As of December 2021, $630 billion had been forgiven. The program was a direct response to COVID and its effect on the economy. In April 2020, employment dropped by 21 million. Stay at home orders and health concerns made it clear that American businesses needed support. Congress moved swiftly to address the public health emergency. They started with the $1.8 trillion Coronavirus Aid, Relief, and Economic Security (CARES) Act. President Trump signed the bill into law on March 27, 2020.

- download PDF here

The CARES Act allocated $367 billion in tax free forgivable loans to small businesses. The PPP’s main goals were to keep workers on employers’ payrolls and ensure the continuity of small businesses. The program was aimed at businesses with 500 or fewer employees, sole proprietors, independent contractors, self-employed, nonprofit organizations, veterans organizations, or tribal business concerns that met the small business criteria. In addition, it afforded establishments in the accommodation and food services sector the same rule to each physical location.

The program allowed businesses to borrow up to 2.5 times their average monthly payroll expense up to $10 million. To make the loan forgivable the borrower needed to allocate at least 60% (originally 75%) of the principal amount to payroll, maintain employee counts and keep compensation to at least 75% pre-COVID levels. Payroll expenses covered wages, bonuses, commissions, payroll taxes, health insurance, and retirement plan contributions.

The government used the banking system to promptly push these grants to businesses. These included federally insured banks, credit unions, farm credit systems and non-bank, non-insured depository institutions such as Community Development Financial Institutions. These loans required no collateral or personal guarantees. Financial institutions were generously compensated to help administer the PPP. Banks received 5% of the principal for loans up to $350 thousand, 3% for loans between $350 thousand and $2 million, and 1% for loans above $2 million. They collected an additional 1% on the portion of any non-forgivable amount. Banks for their part bared no risk and the loans had no effect on their capital requirements. The Brookings paper by Glenn Hubbard and Michael Strain provides an extensive description of the program (see endnotes).

The PPP ran out of money two weeks into its existence. On April 24, President Trump signed into law the $484 billion Paycheck Protection Program and Health Care Enhancement (PPPHCE) Act that allocated $320 billion to the PPP. By the end of May, the PPP ran out of funds once again. On December 27, President Trump signed into law the $2.3 trillion Consolidated Appropriations Act of 2021 that allocated $325 billion for the PPP. In the summer of 2021, the PPP ended. Texas small businesses made 931 thousand applications for $62 billion in PPP forgivable loans. For comparison, California (population 10 million above Texas) had 1.3 million small business applicants borrow $103 billion and Florida (population 8 million below Texas) had 980 thousand applicants borrow $50 billion. Stated differently, the average PPP loan in California was $81 thousand and Florida $51 thousand. Texas landed in the middle with an average of $67 thousand.

In this report, we turn our attention to the reach of the PPP in the Lone Star State. We show that there was broad participation by in state and out-of-state financial institutions. Further, we show that regional banks played an important role in support of their communities. Overall, we note that the PPP helped strengthen the resiliency of Texas small businesses and provided support to community banks.

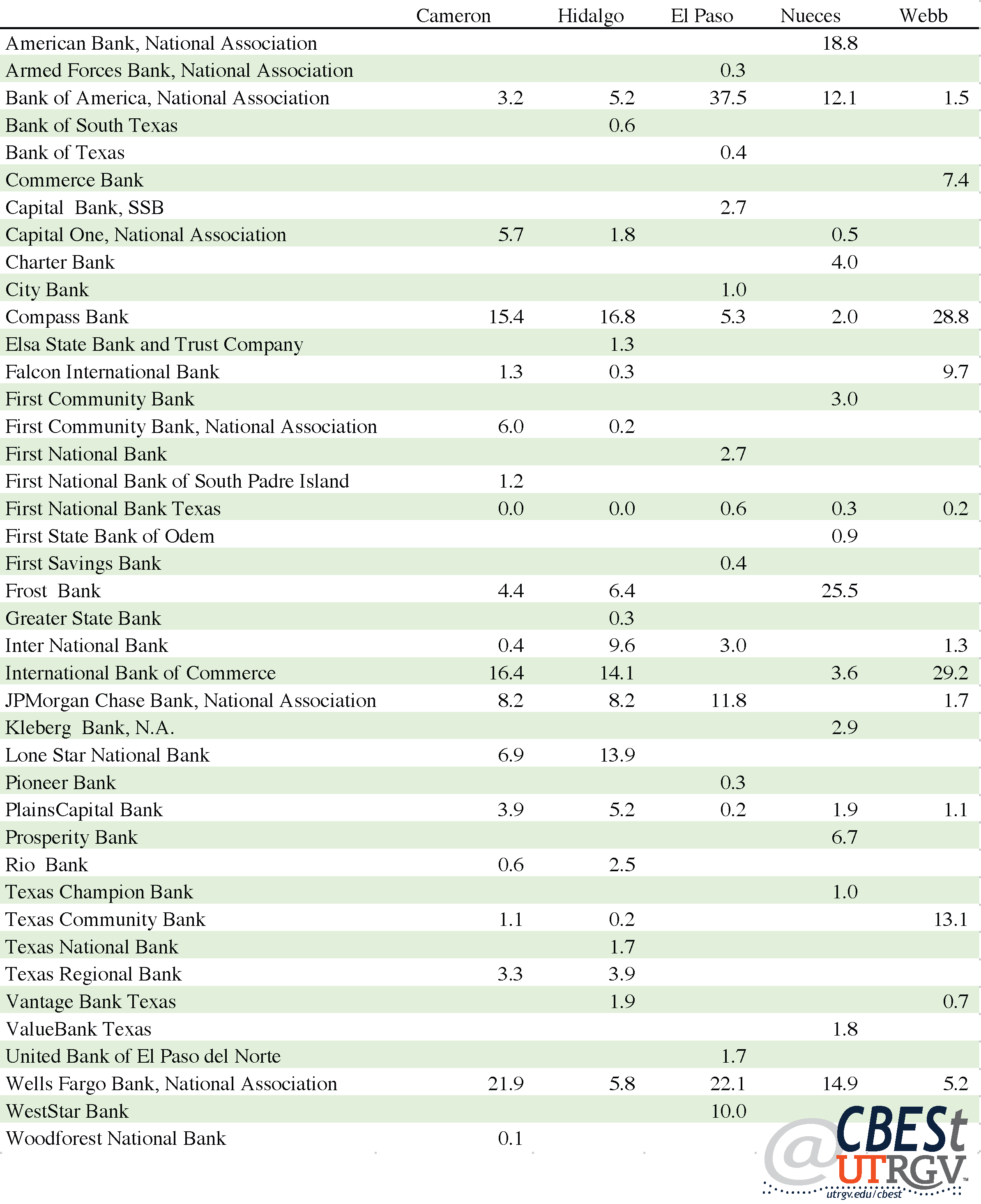

Texas

The PPP had broad participation from the financial community. Some 5 thousand financial institutions took part in the endeavor. JP Morgan Chase, Bank of America, and PNC Bank were responsible for 10% of total US applications valued at $97 billion or 12% of total.

Table 1 presents the top 10 lenders to Texas small businesses by value. These 10 banks handled $20.7 billion in applications or 33% of all the PPP Texas loans. Of these, Frost Bank, Prosperity Bank, Allegiance Bank, and Comerica Bank are based in the Lone Star State. Frost Bank was responsible for $4.6 billion or 7.4% of the state’s total. Not surprising, Texas banks mostly lent to Texas businesses, except Comerica Bank. Of Comerica Bank’s $4.9 billion loans, 81% were to non-Texas small businesses.

Texas accounted for 6% of Bank of America and 7% of Wells Fargo Bank’s PPP loans (second and third largest US banks). Cross River Bank of New Jersey was the 7th largest Texas PPP lender. Cross River Bank, with only 1 branch, was able to leverage its small size and entrepreneurial abilities to take full advantage of PPP. In Q4 2019, Cross Rivers Bank had $2 billion in assets. By Q3 2021 (most recent), total assets were up 5-fold to $11.5 billion. Cross River Bank made 8% of its $14.4 billion in PPP loans to Texas small businesses. It also had the most profound reach of any top lender in the state. Cross River Bank made loans to 1,247 Texas zip codes. For comparison, Frost Bank, the state’s largest producer, made loans to 875 zip codes. Allegiance Bank and Comerica Bank concentrated their loans on the fewest number of zip codes, 385 and 512 respectively.

The last column of table 1 presents the estimated revenue each bank earned disbursing the PPP to Texas small businesses. We use the fee structure discussed above to create bank revenue estimates. Our computation may overstate the true revenue amount by including approved PPP loans that did not materialize and understate for the portion of loans that are not forgivable. The top 10 PPP lenders earned $759.4 million. JP Morgan Chase Bank (the largest US bank) took the top spot at $157.8 million followed by Frost Bank at $156.3 million.

| Table 1: Texas top 10 PPP lenders by value Source: Small Business Administration |

| Lender | Home State | Loans (billions) | Share of Texas loans | Share of Bank loans | Loan applications (thousands) | Texas zip codes | Est. revenue (millions) | |

| 1 | Frost Bank | TX | $4.6 | 7.4% | 99% | 32.1 | 875 | $156.3 |

| 2 | JPMorgan Chase Bank | OH | $4.2 | 6.8% | 10% | 47.3 | 1045 | $157.8 |

| 3 | Bank of America | NC | $2.2 | 3.6% | 6% | 37.4 | 1044 | $86.6 |

| 4 | Zions Bank | UT | $1.9 | 3.1% | 19% | 13.6 | 660 | $60.2 |

| 5 | PNC Bank | DE | $1.9 | 3.0% | 9% | 16.1 | 931 | $64.0 |

| 6 | Prosperity Bank | TX | $1.8 | 2.9% | 90% | 17.2 | 1057 | $67.1 |

| 7 | Cross River Bank | NJ | $1.1 | 1.8% | 8% | 47.9 | 1247 | $53.2 |

| 8 | Allegiance Bank | TX | $1.1 | 1.7% | 99% | 9.9 | 385 | $41.0 |

| 9 | Wells Fargo Bank | SD | $1.0 | 1.6% | 7% | 24.5 | 1123 | $43.7 |

| 10 | Comerica Bank | TX | $0.9 | 1.5% | 19% | 5.1 | 512 | $29.4 |

| Total | $20.7 | 33% | 251.0 | $759.4 |

Figure 1 presents average PPP loans by zip code. The zip code at the 50th percentile had average loans of $58 thousand. The four shaded areas show the distribution of PPP loans across the state. Rural Texas for the most part sits at both extremes of the loan distribution. For example, zip code 79839 in Hudspeth County had 15 applications with an average loan of $21,000. The largest loan went to Hillcrest Dairy for $62 thousand (WestStar Bank) and the smallest loan to Heart JM Transportation for $4 thousand (PeopleFund). Zip code 79837, also in Hudspeth County (crosses into New Mexico), had 14 applications with an average loan of $91 thousand. The largest loan went to Dell Telephone for $882 thousand (Live Oak Banking Company) and the smallest loan to Richard Archuleta for $3 thousand (Capital Plus Financial).

|

| Figure 1: Average PPP loan by zip code Source: Small Business Administration |

The figure also shows that a concentration of above average PPP loans went to Texas largest metros of Austin, Dallas, Houston, and San Antonio. In addition to the metros of Laredo, Corpus Christi, and Beaumont.

Large Metros

Table 2 presents the top 5 lenders in Texas largest metros. The metros are presented in alphabetical order. Austin metro is made up of Bastrop County, Caldwell County, Hays County, Travis County, and Williamson County. The top lender in Austin was Frost Bank, making 4.1 thousand loans with an average face value of $133 thousand. Among the top 5 banks, Horizon Bank, based in Austin, had the higher average at $166 thousand. The top 5 banks made 34% of all loans. The 19 remaining banks headquartered in Austin made an additional 9% of all metro loans. In all, Austin small businesses applied for $5.5 billion to 904 banks.

| Table 2: Texas large metros, top 5 PPP lenders by value Source: Small Business Administration |

| Lender | Home MSA | Loans (millions) | Share of MSA loans | Loan applications (thousands) | Average loan (thousands) | Est. revenue (millions) | |

| Austin Metro | |||||||

| 1 | Frost Bank | San Antonio | $550.1 | 10.0% | 4.1 | $133.3 | $20.0 |

| 2 | JPMorgan Chase Bank | OH | $530.5 | 9.6% | 5.5 | $96.1 | $19.5 |

| 3 | Horizon Bank, SSB | Austin | $306.0 | 5.6% | 1.8 | $166.0 | $11.5 |

| 4 | Bank of America | NC | $240.9 | 4.4% | 4.0 | $59.8 | $9.9 |

| 5 | PNC Bank | DE | $224.1 | 4.1% | 1.9 | $118.1 | $7.9 |

| Rest of metro banks | Austin | $473.0 | 8.6% | 6.9 | $69.0 | $18.7 | |

| All other banks | $3,179.8 | 57.8% | 46.2 | $68.9 | $119.0 | ||

| Dallas Metro | |||||||

| 1 | JPMorgan Chase Bank | OH | $1,705.9 | 8.9% | 18.5 | $92.4 | $62.2 |

| 2 | Frost Bank | San Antonio | $1,390.0 | 7.3% | 8.9 | $156.4 | $45.8 |

| 3 | Bank of America | NC | $847.9 | 4.4% | 14.7 | $57.7 | $33.5 |

| 4 | PNC Bank | DE | $596.7 | 3.1% | 5.3 | $112.1 | $20.6 |

| 5 | Prosperity Bank | El Campo TX | $521.3 | 2.7% | 4.6 | $113.8 | $18.9 |

| Rest of metro banks | Dallas | $5,289.7 | 27.7% | 53.4 | $99.0 | $190.0 | |

| All other banks | $8,718.5 | 45.7% | 165.5 | $52.7 | $324.4 | ||

| Houston Metro | |||||||

| 1 | JPMorgan Chase Bank | OH | $1,521.0 | 8.5% | 17.4 | $87.7 | $56.9 |

| 2 | Zions Bank | UT | $1,497.0 | 8.4% | 10.6 | $141.5 | $47.3 |

| 3 | Frost Bank | San Antonio | $1,154.0 | 6.5% | 6.6 | $173.9 | $37.4 |

| 4 | Allegiance Bank | Houston | $1,010.7 | 5.7% | 9.3 | $108.5 | $38.7 |

| 5 | Bank of America | NC | $773.8 | 4.3% | 12.3 | $62.7 | $29.3 |

| Rest of metro banks | Houston | $2,606.0 | 14.6% | 26.0 | $100.2 | $98.1 | |

| All other banks | $9,312.7 | 52.1% | 194.8 | $47.8 | $353.3 | ||

| San Antonio Metro | |||||||

| 1 | Frost Bank | San Antonio | $988.2 | 22.6% | 7.9 | $124.7 | $34.9 |

| 2 | Broadway National Bank | San Antonio | $411.5 | 9.4% | 2.9 | $142.2 | $14.5 |

| 3 | Texas Partners Bank | San Antonio | $222.4 | 5.1% | 1.2 | $184.8 | $7.6 |

| 4 | JPMorgan Chase Bank | OH | $182.3 | 4.2% | 2.3 | $80.7 | $7.1 |

| 5 | Jefferson Bank | San Antonio | $159.1 | 3.6% | 1.2 | $133.9 | $6.1 |

| Rest of metro banks | San Antonio | $355.4 | 8.1% | 6.8 | $52.0 | $14.9 | |

| All other banks | $2,053.8 | 47.0% | 38.3 | $53.6 | $78.4 | ||

Dallas metro is made up of Collin County, Dallas County, Denton County, Ellis County, Hood County, Hunt County, Johnson County, Kaufman County, Parker County, Rockwall County, Somervell County, Tarrant County, and Wise County. JP Morgan Chase was the top PPP producer in the Dallas and Houston metros. It was second in Austin and fourth in San Antonio. Dallas top 5 banks do not include a bank headquartered in the metro. Comerica Bank was $19 million short to make the top 5 list. Dallas metro had 62 participating financial institutions that are headquartered there. These banks produced 27.7% of all metro loans worth $5.3 billion. Dallas was the largest destination of PPP loans among the selected metros, worth $19 billion.

Houston metro is made up of Austin County, Brazoria County, Chambers County, Fort Bend County, Galveston County, Harris County, Liberty County, Montgomery County, and Waller County. Houston small businesses applied for $18 billion, 33% of which was produced by the top 5 banks. The remaining 42 financial institutions headquartered in the metro produced $2.6 billion or 14.6% of total. The top home institution, Allegiance Bank, produced $1 billion in loans earning it $38.7 million.

San Antonio metro is made up of Atascosa County, Bandera County, Bexar County, Comal County, Guadalupe County, Kendall County, Medina County, and Wilson County. Of the four metros in table 2, only San Antonio was home to most of its top producers. Frost Bank, Broadway National Bank, Texas Partners Bank, and Jefferson Bank were responsible for 40.7% of all metro loans. These banks also had among the highest average loans compared to top 5 producers at the other metros. For example, Frost Bank average loan was $133 thousand, $156 thousand, $174 thousand, and $125 thousand in the Austin, Dallas, Houston, and San Antonio metro, respectively. The 12th largest producer, Vantage Bank Texas, had the highest average loan among San Antonio based banks at $223 thousand.

South Texas and Border Region

Table 3 presents the top 5 lenders in the Corpus Christi and Border metros. The metros are presented in alphabetical order. The Corpus Christi metro is made up of Aransas County, Nueces County, and San Patricio County. The top 5 lenders in Corpus Christi produced $446 million in PPP loans or 56.7% of total. The 5-remaining metro-based financial institutions made an additional $103 million or 13.1% of total. Texas based banks were responsible for 69.7% of all metro loans. Among metro-based banks, Texas Champion Bank (#8) produced the highest average loan and Navy Army Community CU (#9) produced the lowest average at $125 thousand and $32 thousand, respectively.

El Paso metro is made up of El Paso County and Hudspeth County. El Paso had 248 financial institutions handle 15.7 thousand applications valued at $982.6 million. El Paso based institutions in the top 5 list accounted for 45.8% of all metro loans. The 3-remaining metro-based institutions (FirstLight FCU, El Paso Area Teachers FCU, and El Paso Collaborative for Community & Economic Development) account for an additional 2% of metro loans. The largest loan was made to Pizza Properties Inc. by WestStar Bank for $7.2 million. El Paso had 108 loans with a value over $1 million and 13.6 thousand loans valued under $100 thousand.

| Table 3: South Texas and Border Region, top 5 PPP lenders by value Source: Small Business Administration |

| Lender | Home MSA | Loans (millions) | Share of MSA loans | Loan applications (thousands) | Average loan (thousands) | Est. revenue (millions) | |

| Corpus Christi Metro | |||||||

| 1 | Frost Bank | San Antonio | $149.6 | 19.0% | 1.3 | $111.3 | $5.2 |

| 2 | American Bank | Corpus Christi | $135.1 | 17.2% | 1.0 | $129.0 | $5.3 |

| 3 | Prosperity Bank | El Campo TX | $72.2 | 9.2% | 0.8 | $88.3 | $3.1 |

| 4 | Kleberg Bank | Kingsville, TX | $46.7 | 5.9% | 0.7 | $68.0 | $1.9 |